This paper has been republished with the kind permission of Hermes Investment Management and was originally published here.

Economics has developed as a science, conveniently forgetting its roots in political philosophy. Unfortunately that ‘science’ is severely dated, and the functioning of the global capital markets has become separated from the real world.

A simple thought experiment throws light on the theoretically correct strategies for a rational saver, but leaves us with unsatisfactory answers. Neglecting the societal context of our saving activity only serves to further isolate the capital markets.

Instead, a self-perpetuating system requires investors to evolve from simple allocators of capital to its steward, with far broader responsibilities. Maximising holistic returns represents practical action of the responsibility by investors, and stretches far beyond creating wealth simply for its own sake.

Introduction

In a lecture I heard some years ago, a philosopher asserted that science tries to answer the question ‘how’, while philosophy tries to answer the question ‘why’. In looking at the corpus of work produced by academics and practitioners on finance, it seems to me that most, if not all, are trying to answer the ’how’ question, but almost none attempt to answer the ‘why’ question.

I think this is because finance as a discipline sees itself as an extension of economics; and economics, since the nineteenth century work of French economists such as Walras¹ and later of Marshall², has been seen in essence as a science, and therefore this preoccupation with the ‘how’ question is a result of a spillover of that assumption.

Arrested development

Scientists, of course, would find the idea of a science that relies on the concept of ‘externalities’ and an attempted aggregation of individuals’ often disparate behaviours and mood shifts to explain why the laws postulated by this science do not seem to work dynamically or universally, somewhat baffling. In his book The Origin of Wealth, Eric Beinhocker relates a meeting between economists and scientists in the mid 1990’s in Santa Fe. What the scientists found most fascinating was how economists took a snapshot of science in the late nineteenth century, applied it to their discipline, then evolved this discipline with scant regards to the huge advances made in science thereafter.

Economics as a discipline has therefore developed within the confines of how science saw the world at that point in time, while science moved on. Thus, economists still talk of ’equilibrium’ – in 1880 all the rage in physics – while scientists today talk of entropy, for example. Perhaps there is also still a misreading of Adam Smith where many students of economics read The Wealth of Nations, but pay less attention to his The Theory of Moral Sentiments which contextualises it, and so fail to place Smith within the context of the moral philosophy of the eighteenth century that believed in the rationality of humans.

The object of this article is not to enter this debate. In the interest of common sense, and because how we perceive economics has a direct bearing on how we perceive financial theory, I would point out that we are all perfectly comfortable in boarding a metal tube with wings to fly because we are confident that outside the context of quantum mechanics, the laws of Newtonian physics, will always apply in the same way and are never affected by ’externalities’.

To me this suggests two facts about the financial system today: First, that it is concerned with something other than economic endeavour to shape and better the conditions of all citizens; and secondly, that there is in the mind of practitioners a separation between the financial system and the society we live in.

However, I would venture that no one would do the same if the laws affecting flight were as ill-fitting, and with the constantly-shifting outcomes, as the laws of economics. Common sense, therefore, tells us the laws of physics are constant, observable and universal, and observation tells us the ‘laws’ of economics are not.

To my mind this argues that we should stop treating economics, and indeed financial theory, as a science and go back to treating it as part of political philosophy. Perhaps by re-examining the ideas of the nineteenth century economist Bastiat’s notion of the ’full picture’³, we begin to make sense of the failures seen in the financial markets in the context of what we can observe today.

Global capital markets separate from real world

The world we live in today is financed by the pool of global savings, some $75 trillion (4), which indirectly or directly controls the remainder of the global capital markets estimated at some $230 trillion (5). It is my contention that much of the dysfunction of the financial landscape today can be traced back to this obsession with answering the ‘how’ question in trying to put capital to use, and its negligence of the ‘why’ question.

The result is that as we continue to try to fit what actually happens in the observable world to our financial and economic theories and laws, we are constantly forced into a reality described in Alice in Wonderland thus: “If I had a world of my own, everything would be nonsense. Nothing would be what it is because everything would be what it isn’t. And contrariwise what is, it wouldn’t be. And what wouldn’t be, it would”!

That the current state of the financial system is somewhat irrational has been pointed to by many more learned and knowledgeable than myself. In his book The End of Alchemy, Mervyn King points out the extraordinary state of banking post the 2008 crisis where the assets of the top 10 banks in the USA accounted for 60% of GDP, while those in the UK amounted to 450% of GDP (6).

In his turn, Professor Kay points out that the size of the world foreign exchange market (latest figures put it at $1,800 trillion) is several times the size of world exports $16 trillion and FDI at $27 trillion(7). To me this suggests two facts about the financial system today: First, that it is concerned with something other than economic endeavour to shape and better the conditions of all citizens; and secondly, that there is in the mind of practitioners a separation between the financial system and the society we live in.

A thought experiment on retirement

In trying to answer the ‘why’ question in relation to the narrow confines of the global savings pool, I would like to propose (as scientists would) a ‘thought experiment’. Let us assume that the only objective of all savers is simply to maximise their wealth to ensure that they have a pot of wealth at the end of their working lives which they can then spend post retirement.

Further, let us assume that savers have no concern other than accumulating sufficient funds throughout their working life to finance the years they believe they will survive in their retirement. In this case they have two possible options. One is to save a portion of their income over the length of their working life (and let us assume that they can do this in an inflation neutral way, perhaps by putting all their savings in gold, since we have to contend with fiat currency today).

Then they would spend the accumulated total over the length of their retirement years. This straight forward scenario is in essence the ‘Joseph’ methodology. It is simply a transfer of wealth from today, at constant prices, to the future. There is no ‘investment’ involved. The other is to try to ‘grow’ their savings in an attempt to increase the final amount at the point of retirement. Rationally, according to the parameters we set out, a saver should not care, how this can be achieved provided she abides by the laws of the land to avoid financial or legal penalty.

This, in essence, is a transfer to finance of Milton Friedman’s economic dictum that the only rational objective of a commercial concern is to increase profit within the parameters of what is legal (8). The saver can then calculate the risk/return on various strategies to determine her optimal outcome for real returns.

We, as citizens, shape the society we live in through our work, our taxes, which finance public policy and through the daily pursuit of our businesses and the way we live our lives.

Logically, one of the best strategies to increase one’s savings would be to gamble in a manner that shifts the odds in her favour. One of the better ways she could do this would be either through a poker bot or with a top-seeded poker player. Why? Because their hit rate runs at approximately 55%(9); the venture is isolated from any externality other than cheating or an inability of the loser to pay out, and more fundamentally because this venture is only concerned with increasing financial wealth, in isolation from all else.

Another, perhaps more readily understandable strategy to the financial industry, would be to try to plug into general economic growth, whenever it occurs. Under such a scenario, the bet would be simply a two-way bet- is the economy growing or is it not? The saver places the bet if the answer is yes and takes it off if the answer is no. This is the logical reduction of the accepted wisdom among the financial academic community that strategy, or allocation, if you will, is where the majority of returns are made.

Using the rationale we outlined in our thought experiment, the saver would only invest if the economy is in a growth phase and revert into inflation neutral cash when it is not. Moreover, since the majority of active managers achieve a hit ratio of 49%, with skilled alpha managers achieving a hit ratio of 51% (according to a 2008 research paper by Inalytics(10)), the bet then becomes “If I can stack the odds of predicting future economic outcomes in my favour, I simply ‘bet’ on the market, rather than pick managers”.

However, since the track record of financial strategists is even worse than that of ‘active’ managers, this approach is still irrational compared to playing poker! As ludicrous as this may seem, the ‘betting’ logic lies at the heart of much of modern financial academic work. We even talk of investments (whether strategic or company specific) as bets. According to this perception, an active manager represents a double bet (picking one that has a hit ratio of 51% and picking an allocator with a hit ratio of 51%) while a passive manager represents a single bet (is the economy going up or down).

The cop out, of course has been that since developed economies have been growing since the end of World War Two, then staying in the market throughout the cycles in a passive strategy will capture the assumed long term upside of economic growth. However, this is irrational for two reasons.

First, a skilled poker player or a poker bot avoids the drawdown of contractionary cycles and thus mathematically accumulates more wealth in the long term. Secondly, there is an implicit assumption that the post WWII world of continued upward trend in economic growth (which is not provable) will continue forever, and thus enters the realm of faith, not rationality.

So, if this is the outcome of rational behaviour, why is the $75 trillion of world savings not directed to a continuous giant global gaming tournament, where there is a better statistical chance of success, and instead it is directed towards ‘investing’ in the economy where there is a far lower chance of success? It could be that the answer is that there simply isn’t enough capacity in the gaming world to satisfy the demand generated by this pool, or perhaps the answer lies elsewhere.

Shaping society

Let us now leave our thought experiment and turn to examining the ‘why’ question. I would like to suggest that the reason we ‘invest’ our savings goes beyond the simple quest for the accumulation of wealth. The reason for such an assertion has to do with the fact that we, as citizens, shape the society we live in through our work, our taxes, which finance public policy and through the daily pursuit of our businesses and the way we live our lives.

I would contend, therefore that our savings form part of this open adaptive system. In other words, the $75 trillion is not separate from the economic-social fabric we live in, but rather an intrinsic part of it. Moreover it is a tool we should use to control it, in the same way that the taxes we pay to finance government initiatives that help shape the direction and structure of our social economy are equally part of it. If we accept this assertion then we arrive at two main reasons as to ‘why’ we invest.

The first is the straightforward accumulation of wealth, by trying to plug into economic growth. But the second, and I would suggest equally important reason, has to do with the shaping of our social economy. We take it as given that our taxes are spent in part to safeguard, nurture and grow our economic social landscape. Therefore, logically, our savings should be also used for the same purpose.

We invest in our economy to help it grow and to help shape it, so that in accumulating our wealth we benefit ourselves as a community of citizens and individually by improving our economic chances with the creation of new industries or the provision of cheaper goods thus improving our general condition etc.

Equally importantly, is an inter-generational concord so that we leave the next generation a viable economic landscape in the same way those who came before us left us with an economic base we could build on. This is in fact an ancient concept described in a Hebrew (and Arabic) parable of Caesar and the old man planting fig trees in the parable.

Why do you bother to plant trees you would never benefit from, asks Caesar? Because those who came before us planted trees for us to harvest and I plant trees for the next generation to harvest, answers the old man11.

Shareholder responsibility and the economic machine

It is clear that the structure of the capital markets have evolved beyond what economic theory thinks they should be. The large corporations of the world no longer raise the majority of the capital they need from shareholders as they did in the 19th century, as Professor Kay so clearly pointed out in his report(12). However, the $69 trillion equity markets(13) do have shareholders and these shares are held as part of their savings, so we have to ask ourselves, what function do these shareholdings fulfil if they no longer fulfil the function postulated by economic theory?

It cannot be that they are simply ‘chips’ in a grand casino, because the logical conclusion of that thought is it is not an efficient way of betting as pointed out above. Furthermore, we end up in a world, as Professor Kay pointed out in his article(14), where the C-suite has the rights of owners and not the shareholders, which starts to sound like the quote from Alice in Wonderland.

This is particularly the case because these corporations, along with governments, control and shape our economic landscape. Their shareholders are citizens in the countries these corporations operate in, own and work for their suppliers, are employees in them and are their customers.

Economically speaking according to the accepted theory pointed out by Professor Kay, this model dictates that savers while owning the shares of these corporations, which collectively have an enormous influence over their lives, have only a tangential relation with them based on dividend pay-outs and their acting as a proxy for a roulette wheel.

Moreover, this perception ignores the fact that the power of the quoted sector goes beyond what may appear at first sight. This is because it includes the banks, which advance much of the loans to the commercial sector (the rest is often advanced by the same savers who own the shares via their bond portfolios), and many of the private equity firms that finance the non-quoted sector. The collective profits and salaries they pay out which form most of the tax base which finances public economic expenditure.

To dismiss, therefore, the function of the quoted sector because the reality does not fit within economic theory, reminds one of the debate between Galileo and the Church theoreticians in Brecht’s play(15). Possibly, the theory should reflect reality and not the other way round. Because of the enormous control quoted companies have over the life of ordinary citizens who own their shares, we must look for the purpose, the ‘why’ if you will, in something other than capital-raising, dividend payout and capital accumulation.

It seems to me that with the maturing of the capital markets, shareholding should serve a different purpose. They should be a tool for savers to exercise their democratic will as owners in directing this economic machine that so influences and shapes their lives and that of society in a way that serves them collectively as well as individually in the long term. This is not an abandonment of the ‘rationalist’ C18th model for investment, but rather an evolution of it. The capital markets system has reached a stage where it is primarily self-perpetuating.

The quoted sector no longer looks to equity markets as the main source to raise capital. The ownership of shares must therefore evolve so that it becomes the conduit for bringing about long term sustainable prosperity for the entire system. If we accept, therefore, that part of the function of share-ownership is control, maintaining these holdings in times of economic contraction starts to make sense in a way that trying to place a directional bet on the economy does not.

Stewardship and advocacy, a social context for investing

However, to accept this precept implies profound changes to the way we invest. It implies that a large part of the reason for investing in quoted companies is stewardship and that in turns brings its own set of issues. How can a disparate group of shareholders, say the members of a fund such as CalPERS agree on what basis they wish to direct the companies they own collectively? Some may want to ban tobacco, some carbon, some may have specific political agendas (the West Bank is a hot topic for example) etc.

The answer, I think lies in thinking beyond specific ‘local’ items and concentrating instead on the ‘big’ issues that so clearly affect human society as a whole. The Brexit vote and the US Presidential election clearly point to a disenchantment of the majority with the way the free market model appears to be working.

Part of that is structural (globalisation, AI etc) and is hard to tackle outside the realm of public policy, but part of it can be tackled through stewardship (fairness – better wages, union rights, diversity, anti-slave labour clauses, governance, executive pay etc). In like manner, the problems that affect humanity as a whole (global warming, water shortage, food disparity) should be tackled partly through public policy and partly through stewardship (awareness of carbon footprint, encouraging energy companies to move to cleaner energy, open architecture or shared resources for food and water technology etc).

Investors collectively end up financing or owning the whole of the economy that they live and work in, so knock on effects which are not apparent when looking at single investments begin to have a profound cumulative effect on them in their totality.

This in turn would change the way we think of investment in markets. Investing in statistical or accounting factors or in HFT would be laid bare for what it is, a bet on a roulette wheel. While investment in beta would only make sense over the cycles if it is coupled with deep long term stewardship, engagement and perhaps controversially for many activists, the end of disposal as a tool of control.

If our concern is to stop carbon emissions, selling the shares does not produce the desired result because the target mining company would still produce coal relying on its index shareholders as their base if a few activists sell their shares. Such a model would allow for the existence of both active and passive management.

A saver would have most of her assets in beta strategies whose main function is control through stewardship to produce a sustainable economic landscape over the long term, and a much smaller portion in active managers. Assuming she can identify active managers with high active share and skill16, who also hold their shares over the long term, and exercise stewardship, but who can make additional gain by picking companies and industries that are growing more than normal, perhaps because of commercial innovation or technology.

The sum of the parts

At this point, we need to go back to the C19th and Bastiat’s dictum about the ‘whole picture’, or secondary and tertiary effects of investment, and his parable of a broken window(17). I would like to suggest that what he was grappling with is that investment has both a direct and observable financial effect, but also secondary and tertiary effects on areas related to that business. If we take his concept as a broad, rather than a literal, one, I believe we can formulate something akin to what we in Hermes term ‘Holistic Returns’. The idea is simple. A single investment can be looked at in a narrow sense as an initial sum put in a venture that returns a specific financial return over time, hence the idea of DCF and CAPM as valuation models.

However, this approach looks at each investment in complete isolation from its surrounding environment, which in a complex open adaptive system seems irrational. Each investment, and the actions it results in, will have a wider ripple effect, both positive and negative. This is already acknowledged in economic theory as the multiplier effect, but we tend to use it for macroeconomics rather than company-specific investment.

However, as pointed to above, investors, collectively end up financing or owning the whole of the economy that they live and work in, so knock on effects which are not apparent when looking at single investments begin to have a profound cumulative effect on them in their totality.

To illustrate this point, allow me to use three examples. In the first example, the investor owns shares in company A. Company A uses perfectly legal methods to pay less tax than it should and as a result its earnings go up and its share price goes up. In a narrow sense, the investor has made an additional economic gain equivalent to that rise. However, she still lives in the same society in which that company operates. Tax revenues for the government are reduced by that amount. That means that either government will need to cut services or raise taxes to make up the difference.

In both cases, the investor loses the gain on the share by her share of the amount of additional tax or reduced service. In other words, by looking at both sides of the ledger, we can demonstrate that such a gain was a mirage. This even applies within the context of companies operating internationally because the saving pool of the world is interconnected in our globalised capital markets.

In the second example, the saver, who is a citizen of the UK, had investments in bank shares in the 2000’s. The ROE for banks was absurdly high and for several years it looked as if she was making a lot of additional gain on her investment in these shares up to the point the UK market (FTSE 100) reached its peak at 6732 in June 2007. Then in 2008 the GFC struck. The net result was a collapse in stock market prices that eroded the value of all shares, not just bank shares, the UK government’s bail-out of the banks, lower interest rates which lowered yields for years, systemic shock and a recession that resulted in years of lost GDP growth (the opportunity cost or broken window pane of Bastiat’s theory). Today, the market is back past the high of 2007 and the saver might assume that at last she has made her money back on her market investment as a whole, (assuming she held on to her investment throughout the period).

I would suggest that such a conclusion is flawed. After all the cost of the crises to the citizens of the UK was £1 trillion. This cost is still borne by the same saver, in her capacity as a citizen, both as additional government debt (of which £16,000 is her personal share and the same amount for every member of her family) and lost economic opportunity in lost growth, as well as lost income from lost yield.

If we deduct this sum from the current level of the market, even after taking into account paid dividends, we find she is at least still some 17% down on her level of wealth in 2007(18)! In other words, by looking at both sides of the ledger, we can demonstrate that the gains made on her banking shares were equally a mirage because she bore the cost of bailing out their risky behaviour in her capacity as a citizen. Let us now assume for the third example that she invests in energy shares.

She might believe that she is making additional economic gain from these investments, but if energy companies, and indeed the rest of the economy do not make substantial changes to their carbon output, the earth will warm by more than 2.0 degrees. This will eventually result in in higher tax bills related to the cost of fighting flooding, higher food bills for consumers and economic and political disruption. By looking at both sides of the ledger, we can postulate that any such additional gains are equally a mirage, since as a citizen she has to bear the negative effects of the investment.

Incorporating secondary and tertiary effects on society

One criticism that can be made of this approach is to say that while we can easily quantify the direct financial gain or loss from any investment, these secondary and tertiary costs are almost impossible to quantify, and therefore, as a qualitative overlay, they remain at best, a woolly concept, at worst unprovable and therefore a totally impractical proposition. However, an economics professor, Dr Armen Papazian, has come up with a perfectly workable quantitative answer(19).

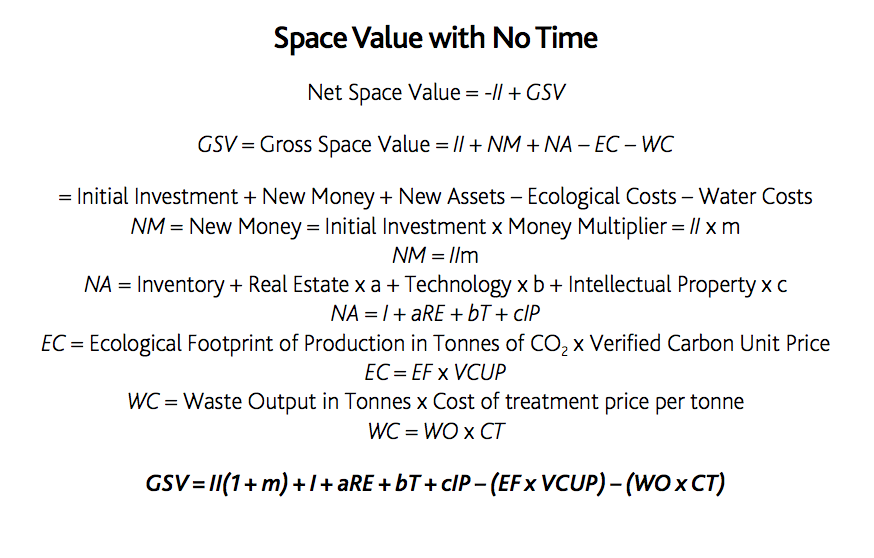

His proposal is to modify the accepted discounted cash flow equation to take into account these other effects. He proposes first that we calculate the effect of our investment on the world we live in on an ongoing basis. We do that by taking the initial investment (II), then take into account new assets that are created which have a wider positive impact, eg buildings, infrastructure, skill development, capex etc (NA) as well as new wealth created, eg from wages paid out, multiplier effect etc (NM), then deduct factors that negatively impact our society, eg carbon footprint (CF) and waste footprint (WF). He called this Gross Space (meaning in the real world) Value, therefore:

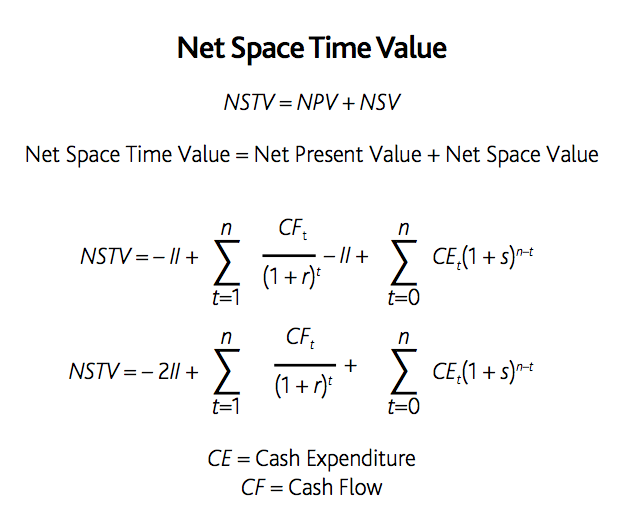

Dr. Papazian then proposes that we arrive at a valuation that looks at both sides of the ledger (he called this Net Space/Time Value or NSTV) by combining the value of what is created and its effects on wider society (both positive and negative) arrived at with the above formula with the traditional net present value calculation of discounted cash flows thus:

Dr. Papazian then proposes that we arrive at a valuation that looks at both sides of the ledger (he called this Net Space/Time Value or NSTV) by combining the value of what is created and its effects on wider society (both positive and negative) arrived at with the above formula with the traditional net present value calculation of discounted cash flows thus:

This may or may not be a perfect answer, but it clearly demonstrates how one can incorporate the idea of calculating the effects of any investment to include secondary and tertiary effects on society within the parameters of traditional financial economics.

We are already beginning to do that in the realm of real estate investment. The development by Lendlease presents the value it created on a multi-million development project in Sydney, not only in terms of financial gain, but also in the fact that it is net water positive, zero net waste producing and net positive in inserting culture and open community space. They are now looking at a similar project in London.

Similarly, at Hermes we talk, not of development, when discussing the largest urban renewal project in Europe in King’s Cross or Paradise in Birmingham, but of place making. We created value in King’s Cross for society by training a whole generation of locals in building skills. We created value for London by providing affordable housing for essential services workers (nurses, firemen, policemen). We created value for the district of King’s Cross by creating the newest London square with the largest water fountain in Europe to provide a shared utility of public space. Our investors therefore not only made a financial return but also benefited as citizens living in London and the UK from such an approach.

I would further like to propose that these secondary and tertiary effects are particularly pertinent to the vast majority of savers, but that their import is not grasped by the financial services community because those who work in financial services are unaware of what may be termed the law of small numbers. People who study and work in finance are comfortable with very large numbers. Asset management companies manage billions or even trillions of dollars. Individual PMs manage hundreds of millions if not billions of dollars. Forex dealers trade in billions if not trillions of dollars and financial engineers are on the lookout to create new innovative products that funnel billions of dollars.

Outside of the asset owner executives, the firms they work for make large margins and they are paid in the top quartile if not top decile of average earnings in their respective countries. They are educated, smart, erudite and mathematically confident.

The truth is that social impacts, the other side of the ledger if you will, have a much more profound impact on the majority of savers whose money the financial services manages, because they earn substantially less and will retire on substantially less, so that well meaning as the industry is, it simply fails to see the world from the perspective of the average saver whose assets it looks after.

The big picture: holistic returns for investors

But, and there is a but, most of the $75 trillion that make up the pool of world savings that fuel the capital markets that shape our global economy and which is controlled by the financial industry are owned by ordinary citizens. They are average workers with average incomes, not the wealthy capitalists of 19th century economics, nor equivalent in earnings to what people in finance earn. We know much about them. 50% are women so we must assume that issues to do with diversity are important to them. Most are employees and often work in the companies they own through their savings or are customers of these companies. Therefore, we know that working conditions, fair pay and fair prices are also important to them.

Most importantly, if they are lucky and live in the developed world they will retire with a lump sum of £300-500 thousand, which translates to about £11-18 thousand per annum income20. At this level of income, certainly in the UK, they cannot cope financially without the additional support of government tax breaks, services and pension of about £4-6 thousand per annum – that is why it is so crucial to them that the collective tax take of the country is not compromised by economic misfortune or specific company action.

Actors in the financial industry work hard for their clients and try to do the best according to the parameters of how they see the world and the financial theory they were taught. Increasing the investment pot for a saver by 10% over and above the required growth rate sounds like a huge and worthwhile goal. And it is – in big numbers when dealing with a pension scheme worth $100 billion, but for the individual saver that is an additional £30 thousand. That would increase the income of our saver from £11,000 to £12,14020 (£30 thousand translated into an annuity) per annum. And we have to ask ourselves the question if that 10% was worth it from a holistic point of view. If we did not use the saver’s assets pooled with others to try to influence companies to reduce carbon emission and the price of water goes up, what use is that additional £95 per month against a water bill which grows at a higher rate than that? If food prices rise because of that, what use is that additional £95 per month for a struggling pensioner already finding it hard to get by?

The truth is that social impacts, the other side of the ledger if you will, have a much more profound impact on the majority of savers whose money the financial services manages, because they earn substantially less and will retire on substantially less, so that well meaning as the industry is, it simply fails to see the world from the perspective of the average saver whose assets it looks after.

I have argued in this paper that the traditional concept that the purpose of investing is only to create additional wealth is flawed when applied to the savings pool today. I argued further that such an approach reduces investment to mere gambling and removes the financial world entirely from the real world investors live and work in. That investing has become a glorified form of gambling on the roulette wheel of the economy is amply illustrated by the trading nature of active funds, the move to index funds, factor investing, derivative instruments, HFT etc, which are all treating the market as a directional bet.

This is further illustrated by the many TV programmes that report on financial markets, minute by minute, tick by tick, like a horse race. I suggested that the role of equity markets has evolved since the capital raising period in the C19th and that it should be redefined as a method for owners to control the companies that control their destiny. I proposed that investing the $75 trillion pool of assets should have a dual purpose of stewardship as well as wealth creation and that all investments should look at ‘both sides of the ledger’ for any investment for the long term. This is holistic return. It is a rational way to invest and to assess the success of our investments, and by applying it we will manage to bring back the financial world from the virtual dislocated place it occupies at present to become relevant to our lives and our future.

The 300 Club The 300 Club is a group of leading investment professionals from across the globe who have joined together to respond to an urgent need to raise uncomfortable and fundamental questions about the very foundations of the investment industry and investing. The mission of the 300 Club is to raise awareness about the potential impact of current market thinking and behaviours, and to call for immediate action. Current economic and investment trends will change the investing landscape over the next two decades and we are at a crisis point which presents huge risks to investors, according to the 300 Club. Moreover, the 300 Club believes that current financial and investment theory and practice run the risk of failing investors at their time of greatest need. www.the300club.org

Footnotes

1 Walras, L., (1874). Elements of Pure Economics, or the theory of social wealth. Lausanne, Paris, 1899 2 Marshall, A., (1890). 1916, Principles of Economics: An Introductory Volume 3 Bastiat, F., (1850). Ce Qu’on Voit et Ce Qu’on ne Voit Pas [What Is Seen and What Is Not Seen], first published as a pamphlet; reprinted in Oeuvres Complètes de Frédéric Bastiat (1873b) Vol 4 Lay, K. (2014). Financing Global Public Goods at Scale. In: Evans, J.W. and Davies, R. Too global to fail : the World Bank at the intersection of national and global public policy in 2025. Washington DC: World Bank Group. p142.

5 Hoogvelt, A. (2012). Globalisation, Risk and Regulation. In: Lauder, H. Educating for the Knowledge Economy?: Critical Perspectives. Abingdon, Oxon.: Routledge. p30 6 King, M., (2016). The End of Alchemy: Money, Banking, and the Future of the Global Economy. WW Norton & Company 7 Kay, J., (2015). Other People’s Money: The Real Business of Finance. PublicAffairs 8 Friedman, M., (1962. 1982), Capitalism and Freedom 9 Levitt, S.D. and Miles, T.J., (2014). The role of skill versus luck in poker evidence from the world series of poker. Journal of Sports Economics, 15(1), pp.31-44 10 Di Mascia, R. and Smith, M. (2008), Research Paper 03: Track Records : Luck or Judgement?, Available at: http://inalytics.com/research-paper-03/ The 300 Club | The Why Question | March 2017 | 3 11 Etz Hayyim Hee – Supplement, p, 3-4 12 Kay, J. (2012). The Kay review of UK equity markets and long-term decision making. Final Report, 9 13 Witkowski, W. (Feb 2015) Global stock market cap has doubled since QE’s start. MarketWatch, available at http://www.marketwatch.com/story/global-stock-market-caphas-doubled-since-qes-start-2015-02-12 14 Kay, J,. (Nov 2015). Shareholders think they own the company – they are wrong. The Financial Times, Available at: www.ft.com/content/7bd1b20a-879b-11e5-90de-f44762bf9896 15 Brecht, B., (1937–39/1943). Life of Galileo (Leben des Galilei) 16 Cremers, K.M. and Petajisto, A., (2009). How active is your fund manager? A new measure that predicts performance. Review of Financial Studies, 22(9), pp.3329-3365 17 Bastiat, F., (1850), Ce qu’on voit et ce qu’on ne voit pas

18 Based on our own calculations 19 Papazian, A. and Nusseibeh, S. (2016), Good Economics shouldn’t cost the earth, Investment Europe. Available at: www.investmenteurope.net/opinion/good-economicsshouldnt-cost-the-earth