It has never been harder to work out whether a financial company is genuinely ethical.

A bank might talk about sustainability, a pension fund might carry an ESG label, and an investment platform might promise to help you build a better future. But what does any of that really mean?

In simple terms, an ethical financial provider should be clear about where your money goes, avoid harmful sectors such as fossil fuels, weapons and tobacco, support positive social or environmental outcomes where possible, and treat customers fairly.

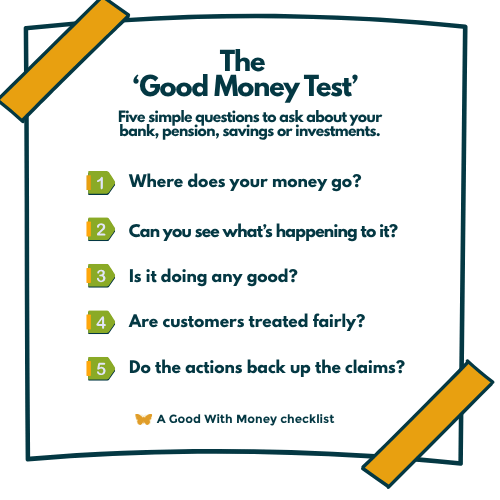

At Good With Money, we’ve created The Good Money Test to help cut through the jargon. It’s built around five simple questions:

The aim is not to make anyone feel guilty about every financial choice. Most of us are juggling cost, convenience, bills, family life and a long list of things we meant to sort out months ago.

This is simply a way to help you spot which providers are genuinely trying to do better – and which ones are mostly talking a good game.

1. Where does your money go?

Financial providers do not just hold your money. Banks lend it, pension companies invest it, and insurers and investment platforms may use it to support a wide range of companies, industries and assets.

That means your money could be helping to fund renewable energy, affordable housing or community businesses. Or it could be linked to fossil fuel expansion, weapons, tobacco, deforestation or companies with poor human rights records.

A genuinely ethical provider should be clear about what it will and will not support. Look for clear exclusions, easy-to-find policies and evidence of where customer money goes. Be cautious of vague claims about “supporting a better future” if there is little detail behind them.

2. Can you see what is happening to it?

Transparency is one of the strongest signs that a provider is serious about ethics.

Some companies publish detailed information about who they lend to, what they invest in and how they measure impact. Others rely on broad sustainability statements with limited evidence.

You should not need to be a fund manager, climate scientist or forensic accountant to understand whether your money is being used responsibly. A good provider should make this information easy to find and easy to understand.

Honesty about limitations can also be a positive sign. No provider is perfect, but customers should be able to see enough to make an informed choice.

3. Is it doing any good?

Avoiding harm matters. But the strongest ethical providers go further.

They actively direct money towards useful social or environmental outcomes, such as renewable energy, social housing, charities, financial inclusion, nature restoration or community businesses.

This is where there can be a difference between a “lower harm” provider and a genuinely impact-led one. For example, a bank that avoids direct fossil fuel project finance may be a better choice than one funding oil and gas expansion. But it is not the same as a bank that actively lends to renewable energy projects, charities or social enterprises.

Both may have a place, and the point is to understand the difference.

4. Are customers treated fairly?

Ethical finance is not only about climate and the environment. A provider also needs to treat customers fairly. That means clear fees, accessible products, responsible lending, decent service and proper support for people in vulnerable circumstances.

Good money should work in real life. It should be understandable, fair and upfront about costs and risks. This is especially important with investments and pensions, where values-led choices still involve risk. An ethical provider should not just inspire you, it should also be straight with you.

5. Do the actions back up the claims?

This is where greenwashing often shows up. A provider might promote a small green initiative while continuing to finance harmful sectors elsewhere. An investment fund might use an ESG label while still holding companies that many customers would not personally consider ethical.

That does not always mean a provider should be written off completely. But it does mean the claims need testing. Red flags include vague language, no clear policy on fossil fuels, big claims based on a small part of the business, selective disclosure or heavy marketing with little evidence.

The key question is: does the provider’s behaviour match the story it tells about itself?

How Good With Money uses the test

When we review providers for our Good List pages, we look at five core areas: money flow, transparency, positive impact, customer fairness and consistency.

This helps us compare different types of providers more clearly. An ethical bank may be assessed on lending policies and fossil fuel exposure. A pension provider may be assessed on fund holdings, climate targets and stewardship. An insurer may be assessed on underwriting, investments and customer treatment.

Not every provider will be strong in every area. Some are brilliant on impact but less competitive on features. Some are convenient and mainstream, but only part-way along the ethical journey.

Our job is to help you see the difference.

The Good Money Test is different from our Good Egg mark. The Good Egg is Good With Money’s independent kitemark for financial providers that meet high standards across people, planet and customers. It is awarded by us after a more detailed review.

The Good Money Test is simpler: it is a reader-friendly checklist anyone can use to ask better questions about a bank, pension, insurer, savings provider or investment platform.

It does not replace the Good Egg, and it is not an accreditation. Instead, it helps explain the kind of thinking that sits behind our Good List pages and shows readers what to look for when judging whether a provider’s ethical claims stack up.

Why the Good Money Test matters

No financial provider is perfect. But the best ethical providers are clear about what they avoid, honest about their limitations and able to show how they use money to support better outcomes for people and planet.

The Good Money Test is not about expecting perfection. It is about helping readers ask better questions – and choose providers that are prepared to answer them.

FAQs

What is an ethical financial provider?

An ethical financial provider is a bank, pension company, insurer, savings provider or investment platform that aims to avoid harmful sectors and, where possible, support positive social or environmental outcomes. This could include avoiding fossil fuel expansion, weapons, tobacco or deforestation, while supporting areas such as renewable energy, social housing, charities or community businesses.

How do I know if my bank is ethical?

Look at what your bank lends to and invests in. Check its fossil fuel policy, exclusions, ownership model, transparency reports and evidence of positive impact. A genuinely ethical bank should clearly explain what it does and does not fund, rather than relying on vague claims about sustainability.

How can I tell if a pension or investment fund is ethical?

Look beyond the fund name. Check the underlying holdings, exclusions, climate policy, voting record and stewardship reports. Some funds labelled ESG may still invest in companies that many customers would not personally consider ethical.

What is greenwashing in finance?

Greenwashing happens when a financial provider makes itself look more sustainable or ethical than it really is. This can include vague green claims, selective disclosure, promoting a small green initiative while continuing to fund harmful sectors, or using ESG language without clear evidence.

Is ESG the same as ethical investing?

No. ESG and ethical investing are related, but they are not the same. ESG usually looks at environmental, social and governance risks that could affect financial performance. Ethical investing may apply stricter values-based exclusions or focus more clearly on positive social and environmental impact.

Does ethical finance mean lower returns?

Not necessarily. Ethical finance does not automatically mean lower returns, but all financial products involve trade-offs. With investments and pensions, returns can go down as well as up, and your capital is at risk.

What is the Good Money Test?

The Good Money Test is Good With Money’s simple checklist for judging whether a financial provider is genuinely ethical. It looks at where your money goes, how transparent the provider is, whether it creates positive impact, how fairly it treats customers and whether its actions match its marketing.