Your pension might not be the most thrilling part of your finances. It’s one of those things we usually ignore until an annual statement lands or we change jobs and get another pot to add to the pile.

But here’s the thing – your pension is likely to become one of the biggest investments you ever have. And while you’re getting on with your life not thinking about it, that money could be backing companies you would never knowingly choose.

That can include oil and gas, mining, arms, tobacco, banks financing fossil fuels, or businesses with poor records on workers’ rights, tax transparency or environmental harm.

The good news is… you have more choice than you might think.

Some providers offer simple, ready-made ethical pensions that do most of the work for you. Others offer self-invested personal pensions (SIPPs), where you can choose your own sustainable funds, ETFs and investment trusts.

The trick is knowing which type is right for you, how hands-on you want to be, and whether the “ethical” label really means what you hope it means.

How we choose the best ethical pensions and SIPPs

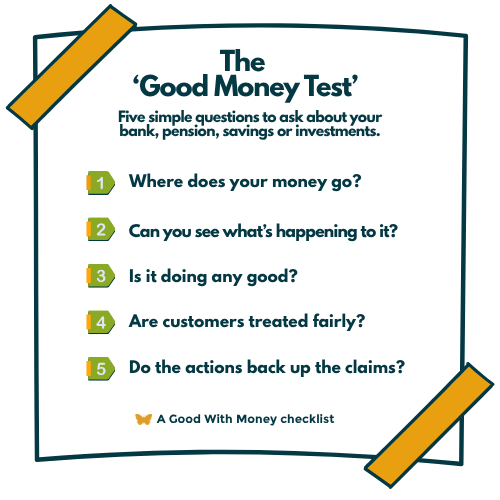

Not all “ethical” or “sustainable” pensions mean the same thing.

That’s why we use The Good Money Test to help assess whether a pension provider is genuinely helping savers align their retirement money with their values, or simply offering a green-looking option on the side.

The test is built around five questions:

Where does your money go?

Does the pension invest in fossil fuels, weapons, tobacco or other harmful sectors? Are there clear exclusions, or can these sectors still appear in the underlying funds?

Can you see what’s happening to it?

Is the provider transparent about the funds it offers, the companies held inside them, and how it measures sustainability or impact?

Is it doing any good?

Does the pension support positive outcomes, such as renewable energy, sustainable infrastructure, healthcare, social housing or companies helping the transition to a lower-carbon economy?

Are customers treated fairly?

Are the fees, charges, investment risks and transfer rules clear? Is the pension easy to understand, especially for people who are new to retirement saving?

Do the actions back up the claims?

Is sustainability built into the pension or platform, or limited to a single ethical fund while the wider business continues to support harmful sectors?

No pension provider is perfect. Some offer strong ready-made ethical plans but limited choice. Others are mainstream SIPP platforms that give you access to sustainable funds, but leave the decisions to you.

The aim is to help you see the difference, so you can choose an option that fits your values, your confidence level and your long-term retirement goals.

Best ethical personal pensions and SIPPs at a glance

| Provider | Type | Best for | Ethical strength | Ethical accreditation / ratings | Watch out for |

|---|---|---|---|---|---|

| PensionBee Climate Plan | Personal pension | Simple fossil fuel-free pension | Strong fossil fuel exclusions and climate focus | Good Egg accredited | Limited investment choice |

| Penfold Sustainable Plan | Personal pension | Self-employed savers | ESG-screened option in an easy digital pension | No formal accreditation found | Less strict exclusions than some specialist ethical options |

| Wealthify Ethical Pension | Managed SIPP | Hands-off ethical investing | Ethical portfolios across different risk levels | No formal accreditation found | Higher fund costs than its Original Plans |

| interactive investor SIPP | DIY SIPP | Sustainable fund choice | Wide access to sustainable funds, ETFs and investment trusts | No platform-level accreditation; depends on fund choice | Investor must choose and monitor holdings |

| Hargreaves Lansdown SIPP | DIY SIPP | Research support | Responsible fund ideas and broad fund choice | No platform-level accreditation; depends on fund choice | Mainstream platform, so ethical outcome depends on your choices |

| AJ Bell SIPP | DIY SIPP | Lower-cost DIY pension investing | Wide access to sustainable and ethical funds | No platform-level accreditation; depends on fund choice | No single ready-made ethical pension plan |

SIPP or personal pension: which is right for you?

A personal pension is a private pension you set up yourself. You can use it if you’re self-employed, want to save outside your workplace pension, or want to combine old pension pots.

A SIPP is a type of personal pension that gives you more control over the investments inside it. That can be useful if you want to pick your own ethical funds, sustainable ETFs, investment trusts or shares.

The trade-off is that more choice means more responsibility. A ready-made ethical pension may suit you better if you want a simple option and don’t want to build your own portfolio.

In simple terms:

A personal pension is usually better if you want an easy, managed option.

A SIPP is usually better if you want wider investment choice and are comfortable making your own decisions.

For many people, the best starting point is still their workplace pension, especially if their employer contributes. But if you are self-employed, have old pensions to combine, or want more ethical control, a personal pension or SIPP can be useful.

What makes a pension ethical?

There is no single definition of an ethical pension. Some funds focus on avoiding harm, while others invest in companies trying to solve social or environmental problems.

Good signs include

Clear exclusions on fossil fuels, weapons, tobacco, gambling or human rights violators.

Transparency on the fund’s full holdings.

Evidence of voting and engagement with companies.

A clear climate policy, not just vague ESG language.

Access to positive-impact funds, such as renewable energy, healthcare, sustainable infrastructure or social housing.

Low exposure to companies expanding fossil fuel production.

The word “sustainable” does not guarantee a fund is fossil fuel-free. It may simply mean the fund manager considers environmental, social and governance factors alongside financial performance.

Best ethical personal pensions and SIPPs in the UK 2026

1. PensionBee Climate Plan

Best for: a simple fossil fuel-free personal pension

PensionBee offers one of the easiest ways to combine old pensions and manage them through an app.

Its Climate Plan is an excellent ethical pension option for people who want to reduce fossil fuel exposure without choosing individual funds themselves. The plan tracks a Paris-aligned index, excludes fossil fuel producers and reduces exposure to carbon-intensive companies.

It also excludes other sectors including controversial weapons, tobacco, gambling, adult entertainment, palm oil and companies that breach the UN Global Compact.

The Climate Plan is not a SIPP in the full DIY sense. You can’t choose your own funds. Instead, you pick from PensionBee’s pension plans and let the provider manage the investments.

That makes it a strong option if you want a straightforward ethical pension, but less suitable if you want complete control.

Fees: 0.75 per cent a year, halved on the portion of your pension over £100,000.

Pros: Clear fossil fuel exclusions, simple app, easy pension consolidation, Good Egg accredited.

Cons: Limited investment choice, 100 per cent equity-based, not an impact-only portfolio.

2. Penfold Sustainable Plan

Best for: self-employed savers and beginners

Penfold is a digital pension provider aimed at making pension saving easier to understand, particularly for self-employed people and small business owners.

Its Sustainable Plan uses ESG-screened investing and offers a simple fee structure. You can set up regular contributions, make one-off payments and combine old pension pots.

The ethical approach is less specialist than some fossil fuel-free or impact-focused funds. The underlying investment approach is based on ESG screening rather than a strict positive-impact mandate, so it is worth checking the current fund factsheet before investing.

Penfold’s simplicity is the appeal. It’s not the deepest ethical option, but it is accessible and easy to use.

Fees: 0.75 per cent a year on savings up to £100,000, falling to 0.4 per cent on the amount above £100,000.

Pros: Beginner-friendly, good for irregular contributions, useful for self-employed savers.

Cons: Less control than a full SIPP, sustainability approach may not be strict enough for some ethical investors.

3. Wealthify Ethical Pension

Best for: a managed ethical pension with risk levels

Wealthify offers a managed personal pension, formally structured as a SIPP, with the option to choose an Ethical Plan.

This is useful if you want your pension managed for you but still want an ethical tilt. You choose your risk level, then Wealthify builds and manages the portfolio.

Its Ethical Plans cost more than its Original Plans because the underlying investment costs are higher. That is worth noting, as pension fees compound over time and can make a meaningful difference to retirement savings.

Wealthify is a good middle ground for people who want a managed ethical pension but don’t want to pick their own funds.

Fees: 0.6 per cent annual management fee on balances up to £100,000, falling to 0.3 per cent on the portion above £100,000. Average investment costs are around 0.58 per cent a year for Ethical Plans.

Pros: Managed portfolio, ethical option, different risk levels, easy to use.

Cons: Higher underlying fund costs for ethical plans, less transparent than choosing funds yourself.

4. Interactive Investor SIPP

Best for: confident investors who want broad sustainable fund choice

Interactive Investor is a DIY investment platform with a flat-fee SIPP. It’s best suited to people who know what they want to invest in, or are willing to do some research.

The main ethical advantage is choice. You can build your own pension portfolio using funds, investment trusts, ETFs and shares. Its ACE 40 list gives investors a filtered selection of sustainable investment ideas, which can be a useful starting point.

This is not the same as the whole provider being ethical. interactive investor is a mainstream platform and the ethical outcome depends on what you choose to hold inside your SIPP.

The flat-fee structure can be good value for larger pension pots, but may be less attractive for very small balances.

Fees: From £5.99 a month for the Core plan, with portfolio limits and SIPP access depending on the plan selected. Check current charges before opening.

Pros: Wide investment choice, useful sustainable fund shortlist, flat fees can work well for larger pots.

Cons: You choose the investments yourself, fees may be high for small pots, not an ethical provider in itself.

5. Hargreaves Lansdown SIPP

Best for: research tools and responsible fund ideas

Hargreaves Lansdown is one of the UK’s largest investment platforms and offers a SIPP with access to a broad range of funds, ETFs, investment trusts and shares.

Its responsible investment hub and Wealth Shortlist include responsible fund ideas selected by its analysts. That can be useful if you want to build your own ethical pension but would like some research support.

The weakness is that the platform itself is broad and mainstream. It gives you access to ethical options, but it also gives you access to plenty of funds and shares that would not meet Good With Money’s ethical standards.

It is best for investors who want research, tools and choice, rather than a ready-made ethical pension.

Fees: Platform and dealing charges vary by investment type and account value. Check current SIPP fees before investing.

Pros: Strong research tools, wide fund choice, responsible fund ideas available.

Cons: More expensive than some DIY rivals, ethical outcome depends on your investment choices.

6. AJ Bell SIPP

Best for: lower-cost DIY pension investing

AJ Bell offers a low-cost SIPP with access to a wide range of funds, shares, investment trusts and ETFs.

For ethical investors, the main benefit is flexibility. You can choose sustainable funds, fossil fuel-free funds, impact funds or ESG ETFs, depending on your values and risk appetite.

AJ Bell is not an ethical specialist, so you will need to do the work yourself. It is a platform rather than a ready-made ethical pension provider.

That said, for investors who are comfortable choosing funds, it can be a cost-effective way to build an ethical pension portfolio.

Fees: AJ Bell’s SIPP platform charge is percentage-based and varies by investment type and value. Fund dealing and share dealing charges may also apply.

Pros: Competitive costs, wide investment choice, good for DIY investors.

Cons: No single ready-made ethical pension plan, requires confidence choosing investments.

Top 5 ethical pension funds in 2026

Is a SIPP more ethical than a workplace pension?

Not automatically. A SIPP gives you more control, which can make it easier to choose fossil fuel-free funds, impact funds or sustainable ETFs. But a poorly chosen SIPP can still hold companies you would rather avoid.

A workplace pension may offer fewer choices, but some schemes now have ethical or sustainable fund options. Before opening a new pension, check whether your current workplace scheme has an ethical fund you can switch into.

You should also think carefully before transferring out of an old workplace pension. Some older pensions have valuable benefits, guarantees or lower charges that you could lose.

Should you transfer your pension to an ethical provider?

Transferring a pension can make sense if you want to combine old pots, reduce fees, improve transparency or move into better ethical investments. But it isn’t always the right answer.

Before transferring, check:

Whether your existing pension has exit fees.

Whether you would lose guaranteed annuity rates or other benefits.

How the new pension’s charges compare.

Whether the ethical option matches your values.

Whether you need financial advice.

How much risk you are taking.

If you’re unsure, speak to a regulated financial adviser before making changes.

Greenwashing risks in ethical pensions

Ethical pensions can still be confusing. Some funds use terms such as ESG, sustainable, responsible, low carbon, climate aware or impact as if they all mean the same thing. They don’t.

A climate-aware fund might still invest in oil and gas companies if the manager believes they are improving. An ESG fund might hold large technology companies with low direct emissions but limited positive environmental impact. A sustainable fund may exclude some sectors but still invest in banks financing fossil fuels.

Good questions to ask include:

Can I see the full list of holdings?

Does the fund exclude fossil fuel producers?

Does it exclude banks financing fossil fuel expansion?

Does it invest in climate solutions or simply lower-carbon companies?

Does it publish voting and engagement records?

Does it have an FCA sustainability label, where relevant?

Does the provider explain why the fund is sustainable in plain English?

If you cannot easily work out what your pension invests in, that is a red flag.

Are ethical pensions safe?

Ethical pensions are regulated in the same way as other UK pensions, but they are still investments. Your money can go down as well as up, and you may get back less than you put in.

Protection also depends on the type of pension and provider. Some personal pensions offered by UK-regulated insurers may have different FSCS protection from SIPPs. With SIPPs, FSCS protection may be capped if the SIPP operator fails, so it is worth checking the exact protection before opening an account.

Ethical does not mean risk-free. It means your pension is trying to invest according to a particular set of values or sustainability criteria.

Which ethical pension is best for you?

If you want a simple fossil fuel-free pension, PensionBee’s Climate Plan is one of the clearest options.

If you are self-employed and want an easy digital pension, Penfold is worth considering.

If you want a managed ethical pension with risk levels, Wealthify may suit you.

If you want to choose your own sustainable funds, look at a SIPP platform such as interactive investor, AJ Bell or Hargreaves Lansdown.

If you want a managed ESG portfolio from a large provider, J.P. Morgan Personal Investing may be an option, but check whether the sustainability approach goes far enough for you.

The right choice depends on how hands-on you want to be, how much you are investing, how strict your ethical criteria are and whether you need advice.

Risk warning

With pensions and investments, your capital is at risk. The value of investments can go down as well as up, and you may get back less than you put in. Pension and tax rules can change, and their value depends on your personal circumstances. This article is for general information only and is not financial advice.