If you’ve got some spare cash once the bills are paid, the first priority should be building an emergency buffer.

Most experts suggest holding three to six months’ essential expenses in an easy-access savings account. That pot isn’t there to make you rich – it’s there to stop you reaching for expensive credit if the boiler breaks, your car fails its MOT or your income suddenly drops.

Cash savings are predictable and protected. Your money won’t fall in value overnight and, up to £120,000 per person per institution, it’s covered by the Financial Services Compensation Scheme (FSCS).

However, inflation almost always means that your cash savings will lose value over time. If you’re saving for goals more than five years away – retirement, a house deposit, financial independence – investing is generally a better way to grow your wealth, though it comes with ups and downs along the way.

If you’re looking to keep some savings in cash, here are some of the more ethical options to consider – from social and environmental pioneers to mutuals that are structurally less driven by shareholder profit.

Best ethical savings accounts: quick comparison

| Provider | Example account | Rate at time of writing | Access | Why we like it |

|---|---|---|---|---|

| Triodos Bank | Everyday Savings | 2.20% AER variable | Instant access | Good Egg mark. A long-standing ethical bank that only lends to organisations delivering positive social, cultural or environmental impact. |

| Triodos Bank | Ethical Savings Bond | 3.60% gross/AER | Fixed term | A fixed-rate option from one of the UK’s clearest ethical banking leaders. |

| Ecology Building Society | Easy Access | 2.30% gross/AER variable | Easy access | Good Egg mark. Uses savers’ money to help fund greener homes and environmental renovation projects. |

| Ecology Building Society | 35-Day Notice | 3.60% gross/AER variable | 35 days’ notice | A stronger rate from a building society with a clear environmental lending mission. |

| Co-operative Bank | Regular Saver | 7.00% AER variable | Monthly saver with restrictions | Long-standing ethical policy. Now owned by Coventry Building Society. Good rate, but check access rules. |

| Nationwide | Flex Regular Saver | 6.50% AER variable | Monthly saver with restrictions | A mutual owned by members, with profits reinvested for customers rather than external shareholders. |

| Coventry Building Society | Regular Saver | 4.63% AER variable | Monthly saver with withdrawal charge | Mutual ownership and B Corp status through the wider Coventry group. |

| Tandem Bank | Instant Saver | Up to 4.45% gross/AER variable | Instant access | Says savings are not used to fund fossil fuel extraction and production. Lending includes greener home improvements. |

| Charity Bank | Easy Access | 3.04% AER | Easy access | Lends savers’ money to charities and social enterprises across the UK. |

| Gatehouse Bank | Woodland Saver | 3.80% to 4.15% AER, depending on term | Fixed term | Sharia-compliant bank with exclusions including alcohol, gambling and weapons. Woodland Saver accounts support tree planting. |

| Raisin UK | Al Rayan one-year fixed-rate bond | 4.65% AER/gross | Fixed term | Savings platform offering access to selected providers, including Sharia-compliant and mutual options. Check the underlying bank before applying. |

| Credit unions | Local savings accounts | Varies | Varies | Community-focused, mutual providers where savings help fund affordable local lending. |

Rates and terms can change quickly. Always check the latest AER, minimum deposit, access rules and FSCS protection before opening an account. Raisin UK is a savings platform rather than a bank, so check which provider your money is held with and whether it is covered by FSCS protection.

How we choose ethical savings accounts

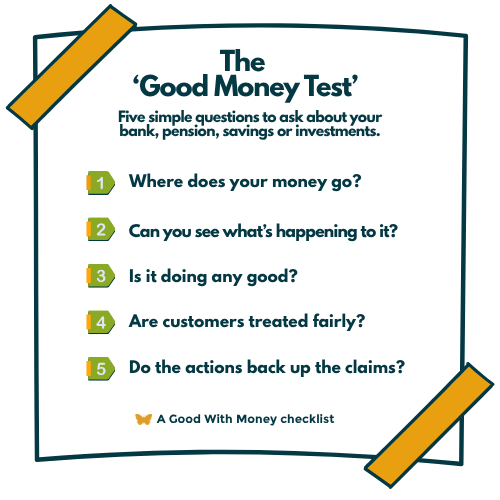

At Good With Money, we use our Good Money Test to help assess whether a savings provider is genuinely aligned with people and planet.

We look beyond the headline interest rate and ask five key questions:

- Where does the money go?

Does the provider lend to fossil fuels, weapons, tobacco or other harmful industries, or does it use deposits to support homes, charities, communities and environmental projects? - How transparent is it?

Can savers easily find out how their money is used, what the provider excludes and what kind of lending or investment it supports? - Does it have a positive impact?

Some providers go further than avoiding harm by actively funding renewable energy, greener homes, social housing, charities, community finance or other positive outcomes. - Are customers treated fairly?

We look at whether the provider offers clear terms, fair access rules and reasonable rates, as well as whether it has a track record of putting customers first. - Do its actions match its claims?

Green language is easy to use. We look for evidence, policies, ownership structures, lending data, accreditation or independent verification to support ethical claims.

Some providers also hold Good With Money’s Good Egg mark, which recognises companies that can show they are making a positive impact. Where a provider has Good Egg accreditation, we have highlighted this in the article.

1. Triodos Bank

- Everyday Savings (instant access): 2.20% AER (variable) on standard accounts.

- Ethical Savings Bonds: 3.60% gross/AER on fixed terms.

- Online Cash ISA: 2.35% tax-free / 2.36% AER.

Why is it ethical?

Ethical Bank Triodos, which has a Good Egg mark from Good With Money, is a true leader in the field of ethical personal finance and only invests in businesses that have a positive social and/or environmental impact.

Key terms

- The Everyday Savings account gives instant access with no notice required. It has a £1 minimum deposit.

- The Ethical Savings Bonds offers fixed rates of one or two years.

2. Ecology Building Society

- Easy Access: 2.30% gross/AER (variable)

- Regular Savings (monthly deposits): 3.00% AER (variable)

- 35-Day Notice: 3.60% gross/AER (variable)

- Rhondda Cynon Taf (RCT) Community Impact Saver Account: 2.30% gross/AER

- Ecology Sea-Changers Impact Saver Account: 2.30% gross/AER

Why is it ethical?

Ecology Building Society is known for its mortgages on eco-friendly new builds and renovation projects. So what it takes in deposits from savers, is used to lend to making Britain’s housing stock more energy efficient.

The company boasts a Good Egg mark from Good With Money, which is awarded only to companies that make a positive impact in the world. It was also the first building society awarded a Fair Tax Mark.

The RCT account makes a monthly donation to the Ecology Community Scheme, while the Sea-Changers account makes a quarterly donation to marine conservation charity Sea-Changers.

Key points

- Membership gives voting rights.

- Accounts help fund planet-positive projects.

3. Co-operative Bank

- Regular Saver paying 7 per cent AER (variable) for 12 months

- Cash ISA and fixed-term options available, but rates vary

Why is it ethical?

The Co-op Bank has a long history of ethical banking, having launched its first ethical policy back in 1992. Now, it is committed to carbon neutral operations, and won’t fund or invest in companies that manufacture or market destructive products like weapons and tobacco. It says it won’t support businesses or organisations that have business relationships with oppressive regimes and will promote human rights and equality across the world.

In 2017 the bank was bailed out by international hedge funds, which dented its reputation for responsibility. However, in 2024 it was bought by Coventry Building Society – a B Corp company with high ethical standards.

Key points

- Regular saver can pay competitive rates – but check access rules.

- Other savings accounts vary widely in rates and access.

4. Nationwide

- Flex Regular Saver: 6.5% AER with monthly saving cap; rate may reduce after extra withdrawals.

- Flex Instant Saver: 2.3% AER (for current account customers).

Why is it ethical?

As a building society, Nationwide must hold at least 75 per cent of its assets in residential property, making it far less likely than its big bank competitors to be lending to unsustainable firms. Its profits are also invested back into the business for the benefit of borrowers and savers (it’s “members”) rather than shareholders.

Key points

- With the Flex Regular Saver, after four withdrawals the interest rate reduces to 1.05 per cent AER/gross a year (variable) for the rest of the term.

5. Coventry Building Society

- The Regular Saver account: 4.63 per cent AER (variable) on monthly savings

Why is it ethical?

Mutual ownership helps align the society’s interests with customers, though executive pay at some mutuals has drawn scrutiny.

Key terms

With the Regular Saver account you can save from £1 to £500 per month. You can access your money, but it’s with a charge equal to 30 calendar days interest on the amount withdrawn.

6. Tandem Bank

- The Instant Saver account: Up to 4.45 per cent interest (variable) gross/AER per year

Why is it ethical?

A digital challenger bank, Tandem aims to be a “greener, more accessible bank for people across the UK”. Tandem guarantees that your savings are never used to fund fossil fuel extraction and production or similar destructive industries. Instead, money held in Tandem savings accounts is used solely to fund its lending products.

Its home improvement loans finance energy-efficient improvements such as solar panels and air source heat pumps, saving people money on energy bills while also helping to save the planet. Tandem’s EPC mortgages reward customers who own energy-efficient homes.

Key terms

- No minimum deposit. Manage your account online. The rate includes a 0.25 per cent “top-up” but this is available at the click of a button.

7. Charity Bank

- Easy access at 3.04 per cent AER

- 33-Day notice account up to 3.04 per cent AER

Why is it ethical?

Charity Bank was founded to support charities with loans that they couldn’t find elsewhere and to show people how their savings could be invested ethically and in ways that would make them happy. It invests its customers’ money into charities and social enterprises around the country.

It says on its website: “Charities have never been more needed, but also more challenged. That’s why our promise – of supporting charitable activities and helping people to save and do good – is more important than ever.”

Top 6 ethical current accounts

8. Gatehouse Bank

- Woodland Saver accounts pay ‘expected profit’ rates (currently 3.80%-4.15% AER depending on term)

Why is it ethical?

As a Sharia-compliant bank, Gatehouse avoids alcohol, gambling, weapons and similar sectors; its Woodland Savers include tree-planting initiatives.

9. Raisin UK

Raisin isn’t a bank but a savings platform that lets you access a range of savings accounts from building societies (often mutual or ethical-aligned) and Sharia-compliant providers.

It can be particularly useful if you want to compare ethical deals, but always check FSCS protection and product terms before committing.

Top ethical offers:

- One year fixed-rate bond with Sharia bank Al Rayan offering 4.65 per cent/AER/Gross

Other ethical savings options

Credit unions

Local credit unions are mutual, community-focused savings/co-ops where your savings fund affordable local lending. Rates vary, and dividends (shared profits) replace traditional interest rates. FSCS protection applies. Check for a credit union near you.

Good With Money occasionally uses affiliate links to providers or offers, where relevant. This means that if you open an account or buy a service after following the link, Good With Money is paid a small referral fee. We choose our affiliates carefully and in line with the overall mission of the site.