International travel continues to grow. An estimated 1.52 billion tourists travelled abroad in 2025, almost 60 million more than the year before, while global arrivals rose again in early 2026.

That brings economic benefits, but it also puts greater pressure on popular destinations already dealing with overtourism, water shortages and increasingly disruptive weather. The latest available figures show that travel and tourism accounted for 7.3 per cent of global greenhouse gas emissions in 2024, with transport responsible for 40 per cent of the sector’s footprint..

Most of us think carefully about where we stay, how we travel and what we spend while we’re away. Travel insurance is easier to overlook, but the provider you choose is also important.

Some brokers donate part of their premiums or commissions to environmental causes. Others support community projects, campaign for fossil fuel divestment or encourage lower-carbon travel. The insurer behind the policy may also invest customers’ premiums before claims are paid, making its climate policies and underwriting decisions relevant too.

The market is still limited, and no option is perfect. But these five ethical and eco-friendly travel insurance choices offer practical ways to direct more of your holiday spending towards businesses trying to do better for people and planet.

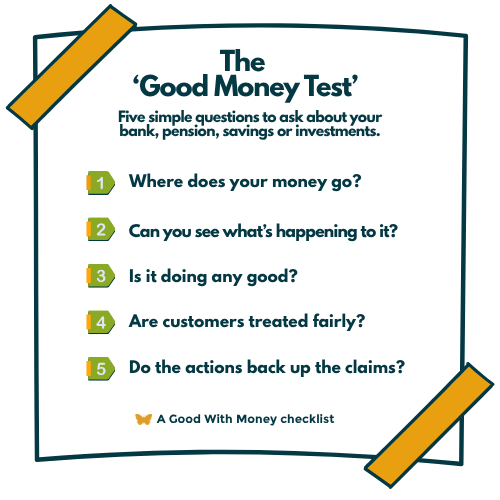

How we apply the Good Money Test to travel insurance

At Good With Money, we use the Good Money Test to look beyond a company’s marketing and consider what happens to customers’ money.

For travel insurance, we ask:

Where does the money go? Does part of the premium or broker’s commission support environmental or social work? Who receives most of the premium?

Is the provider transparent? Can you identify the broker, insurer and underwriter, along with any charitable contribution?

Is it doing measurable good? Are donations automatic and clearly reported, or does the positive impact depend on the customer contributing extra?

Are customers treated fairly? Does the policy provide suitable medical, cancellation and repatriation cover, with understandable limits and exclusions?

Do its actions match its claims? Does the company campaign for change, restrict harmful investments or underwriting, and publish evidence of its impact?

The underwriter is key because it usually receives most of the premium, invests insurance funds and pays claims. Ethical Consumer’s 2025 travel insurance research found that ethical choice among major underwriters remained weak, with many scoring poorly on climate, investment and transparency measures.

No option here is perfect. The aim is to find suitable cover while making a better-informed choice about the company selling it and the insurer behind it.

Naturesave

Best for: the clearest overall ethical commitment

Naturesave is a long-established ethical insurance broker based in Devon. It donates 10 per cent of home and travel insurance premiums to the Naturesave Trust, which supports small environmental and conservation projects across the UK. The broker and trust have directed more than £1 million towards environmental work since Naturesave was founded.

Its commitment extends beyond donations. Naturesave has campaigned for the insurance industry to stop supporting fossil fuel expansion and introduced paid additional leave for employees choosing slower, lower-carbon journeys instead of flights.

Naturesave became part of Benefact Group in 2022. Benefact is owned by a charitable trust and gives all available profits to charities and good causes, giving Naturesave an ownership structure that supports its wider mission.

Its personal travel insurance is offered with AXA. This creates an important caveat: Naturesave’s own business and charitable model have strong ethical credentials, but the policy is ultimately backed by a large mainstream insurance group.

What we like: The charitable contribution is built into the model rather than added by the customer. Naturesave also has a long record of environmental campaigning and transparent giving.

What to check: Read the policy wording closely, particularly for pre-existing conditions, trip disruption, natural disasters, maximum journey lengths and optional activities.

Evergreen Insurance Services

Best for: choosing which environmental charity benefits

Evergreen is a family-run ethical insurance broker that donates part of the commission it earns to wildlife, animal welfare and environmental charities.

Customers can choose which partner charity receives the money. Evergreen says it donates up to 25 per cent of its commission, with some arrangements rising from 10 per cent in the first year to 15 per cent in the second and 25 per cent from the third year.

Its travel insurance quote service currently connects customers with Just Travel Cover and SunWorld, which provide single-trip and annual policies. The insurer and underwriting arrangements can vary according to the product offered, so check the policy documents rather than assuming Evergreen itself provides the cover.

What we like: Customers have a direct say in which organisation receives the donation. Evergreen is also clearer than many businesses about the fact that the contribution comes from its commission.

What to check: “Up to 25 per cent” is not necessarily the amount donated from a new policy. It is also a percentage of Evergreen’s commission, not of the full insurance premium. Check the underwriter attached to your quote and whether its policies match your values.

World Nomads

Best for: backpackers, independent travellers and adventurous trips

World Nomads specialises in insurance for independent and adventurous travellers. Its policies can cover more than 150 sports and activities, although the exact activities included depend on the policy and country of residence.

Customers buying a policy can make an optional micro-donation through the Footprints programme. They choose from current projects addressing issues such as poverty, education, equality and wildlife conservation. World Nomads says 100 per cent of each donation goes to the selected project.

The programme has raised around A$3.6 million (around £1.9 million) for community development projects. World Nomads also produces guidance on responsible tourism, wildlife encounters and travelling with less waste.

For UK customers, World Nomads policies are underwritten by Collinson Insurance, a trading name of Astrenska Insurance Limited. World Nomads forms part of the Australian nib Group.

What we like: The Footprints programme is transparent about where donations go, and World Nomads offers cover aimed at travellers whose planned activities may not fit a basic policy.

What to check: The positive contribution is optional and comes from the customer, rather than being funded automatically from every premium. Its mainstream parent and underwriter should also form part of your decision.

One Tree Travel

Best for: travellers with medical conditions who want an automatic environmental contribution

One Tree Travel is a trading name of Freedom Insurance Services, an established UK travel insurance intermediary with experience of arranging cover for people with pre-existing medical conditions.

It funds at least one tree through Ecologi for every travel insurance policy sold. The contribution is made within 30 days of purchase, and customers can view its publicly available tree-planting record.

One Tree Travel offers single-trip and annual cover, with medical screening for existing conditions. Depending on the policy selected, cover can include up to £10 million for emergency medical treatment and repatriation and up to £10,000 for cancellation and curtailment.

The company offers policies backed by several insurers, including Allianz Partners, Starr International Europe and Accelerant Insurance UK. The underwriter therefore depends on the quote and policy selected.

What we like: The tree contribution happens automatically, and the company provides a visible record of the projects it funds. Its focus on medical conditions could also make it useful to travellers who struggle to find suitable mainstream cover.

What to check: Funding one tree is a modest environmental contribution and does not, by itself, make the insurer or policy fully sustainable. Check which underwriter is offering your quote and look at its investment and fossil fuel policies.

Responsible Travel and Columbus Direct

Best for: combining a discount with a charity donation

Responsible Travel is a sustainable holiday company rather than an insurer. It has a partnership with Columbus Direct through which customers receive a 20 per cent discount on standard Columbus travel insurance rates.

Customers can keep the full discount, donate it to charity, or divide it between themselves and a participating cause. Organisations supported through the arrangement have included the World Cetacean Alliance, Elephant Family and Surfers Against Sewage.

Columbus Direct offers single-trip, annual, backpacker, family and specialist policies. Depending on the cover level, policies can provide up to £15 million for emergency medical expenses and repatriation, up to £5,000 for cancellation and up to £2,500 for baggage.

Columbus Direct is a trading name of Collinson Insurance Services, and its UK policies are underwritten by Astrenska Insurance Limited. This is the same underwriting group used by World Nomads in the UK.

What we like: It gives customers control over the balance between saving money and supporting charity, while linking insurance with a business that promotes locally owned and lower-impact travel.

What to check: The charitable element comes from giving up some or all of your discount. The insurance product itself is a conventional Columbus Direct policy, so this is better described as a responsible purchasing route than a distinctly ethical insurance policy.

Which ethical travel insurance option is best?

For the strongest company-wide ethical credentials, Naturesave is our top choice. Its environmental giving is automatic, it has a long campaigning record, and it sits within a charity-owned financial group.

Evergreen is worth considering if you want to select the wildlife or environmental charity supported by your policy.

World Nomads may be more suitable for backpackers and travellers planning a wider range of activities.

One Tree Travel could suit people with pre-existing medical conditions who also want each purchase to fund an environmental project.

Responsible Travel’s Columbus partnership is a practical option for customers who want to donate part of an insurance discount to charity.

The right answer still depends on the cover. An ethical policy that excludes your medical condition, destination or planned activity is unlikely to be a sensible purchase.

What to check before buying travel insurance

Travel insurance is primarily intended to meet potentially high emergency medical and repatriation costs. It may also cover cancellation, baggage and disruption, but the limits and exclusions vary considerably.

Check:

- the medical and repatriation limit

- whether all existing medical conditions have been declared and accepted

- cancellation cover against the full cost of your booking

- natural disaster and travel disruption cover

- baggage, gadget and single-item limits

- excesses for each person and each section of a claim

- maximum trip lengths and age restrictions

- cover for cruises, winter sports or adventurous activities

- the policy’s treatment of official travel advice

Do not assume that wildfires, floods, extreme heat or airport closures are automatically covered. The Association of British Insurers says natural disaster or disruption claims generally depend on the policy including the relevant cover. Travellers must usually seek refunds from airlines, accommodation providers or tour operators before claiming from insurance.

Buy insurance as soon as you book, rather than waiting until departure. Cancellation cover generally begins when the policy starts, so delaying could leave the cost of your holiday unprotected.

Ethical travel insurance FAQs

What is ethical travel insurance?

Ethical travel insurance is cover sold by a company that considers its environmental and social impact. This might include donating part of premiums or commission, supporting community projects, avoiding harmful investments, campaigning for lower-carbon travel or operating under charitable ownership.

Is there a fully ethical UK travel insurer?

There is no obvious perfect option. Most specialist ethical providers are brokers that place policies with mainstream underwriters. Naturesave has particularly strong credentials as a broker, but its travel policy is offered with AXA.

Does ethical travel insurance cost more?

Not necessarily. Prices depend mainly on age, destination, trip length, medical history and the amount of cover required. Compare the total cover and excesses rather than choosing solely on price or charitable giving.

Does travel insurance cover climate-related disruption?

Sometimes. Cover for wildfires, floods, severe weather and other natural disasters varies by policy and may be an optional addition. Check the wording for natural disaster, catastrophe and travel disruption cover before buying.

Does planting trees make travel insurance sustainable?

Tree planting can support ecosystems and local communities, but it does not erase the emissions from a holiday or prove that an insurer has responsible investment and underwriting policies. It should be treated as one factor in a wider assessment.

Why does the underwriter matter?

The underwriter receives much of the premium, carries the insurance risk, pays valid claims and may invest large pools of customers’ money. Checking the underwriter gives a fuller picture than looking only at the brand or broker selling the policy.