| What is an ethical current account? An ethical current account is an everyday bank account that aims to avoid funding harmful industries – like fossil fuels, arms or tobacco – and, in some cases, actively support positive environmental or social outcomes. |

If you’re looking for a quick answer, these are some of the best ethical current accounts in the UK right now, based on transparency, lending policies and impact:

- Triodos Bank: a fully impact-led bank and the benchmark for ethical banking

- The Co-operative Bank: long-standing ethical policy with mainstream features

- Nationwide Building Society: member-owned with improving sustainability, though not purely ethical

We’ll walk through each option below.

Why ethical banking matters

Banks don’t just hold your money – they use it.

That means your current account balance can help fund anything from renewable energy projects to fossil fuel expansion.

Recent data shows major banks are still heavily financing oil and gas. For example, Barclays provided $35.4 billion (£26.26 billion) in fossil fuel financing in 2024, according to the Banking on Climate Chaos report.

For many people, that raises the question: is there a better option?

The answer is yes – and switching is easier than you might think, thanks to the Current Account Switch Service.

How we choose the best ethical current accounts

Not all “green” claims mean the same thing.

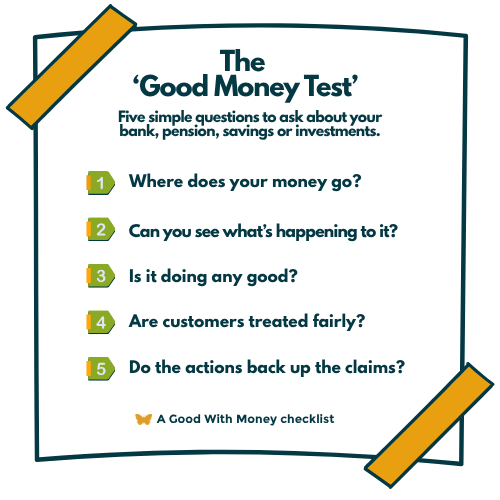

That’s why we use The Good Money Test to help assess whether a bank is genuinely trying to do better, or mostly talking a good game.

The test is built around five questions:

- Where does your money go?

Does the bank fund fossil fuels, weapons, tobacco or other harmful sectors? - Can you see what’s happening to it?

Is the bank transparent about who it lends to, what it avoids and how it measures impact? - Is it doing any good?

Does it actively support positive outcomes, such as renewable energy, social housing, charities or community businesses? - Are customers treated fairly?

Are fees, features, overdrafts and customer protections clear and fair? - Do the actions back up the claims?

Are ethics embedded across the business, or limited to a small green initiative or marketing campaign?

No bank is perfect. Some are fully impact-led but have fewer features. Others are more mainstream but still offer a better option than the biggest fossil-fuel funders. The aim is to help you see the difference.

Best ethical current accounts in the UK (2026) – at a glance

| Provider | Monthly fee | Fossil fuel exposure | Positive impact focus | Overdraft | FSCS protected | Ethical accreditation | Best for |

|---|---|---|---|---|---|---|---|

| Triodos Bank | £3 | None | Strong (core mission) | No | Yes | Good Egg | Full impact-led banking |

| The Co-operative Bank | £0-£15 | No direct project finance | Moderate | Yes | Yes | B Corp (via Coventry Building Societyownership) | Ethical high street option |

| Nationwide Building Society | £0-£18 | Indirect | Moderate (e.g. social housing) | Yes | Yes | – | Mutual with mainstream features |

| Cumberland Building Society | £0 | None | Limited (local focus) | Yes | Yes | – | Local, simple banking |

| Starling Bank | £0 | No direct project finance | Limited | Yes | Yes | – | Digital banking with low exposure |

1. Triodos Bank

- Monthly fee: £3

- Fossil fuel exposure: None

- Positive impact investment: Yes

- Overdraft: No

- FSCS protected: Yes

- Good With Money Good Egg: Yes

Triodos remains the gold standard for ethical banking in the UK. It only lends to organisations with clear social, environmental or cultural benefits – and uniquely, it published every organisation it finances.

That level of transparency is rare. The trade-off is fewer features, such as no arranged overdraft.

Best for: Those who want their money to actively fund positive change.

Read our full review of Triodos Bank

How to divest your money from fossil fuels

2. The Co-operative Bank

- Monthly fee: £0 – £15

- Fossil fuel exposure: No direct project finance

- Positive impact investment: Some

- Overdraft: Yes

- FSCS protected: Yes

The Co-operative Bank has one of the longest-running ethical policies in UK banking, shaped by customer input.

It avoids funding fossil fuel extraction and arms, while offering the kind of everyday features you’d expect from a high street bank.

It’s now owned by Coventry Building Society, which is a certified B Corp.

Best for: Ethical values with full-service banking.

The UK’s most ethical banks and building societies

3. Nationwide Building Society

If you’re a member, you can switch your main account to Nationwide’s FlexPlus, FlexDirect or FlexAccount using the Current Account Switch Service online and get £200. Ending 10 July.

- Monthly fee: £0 – £18

- Fossil fuel exposure: Indirect (via Virgin Money acquisition)

- Positive impact investment: Yes (e.g. social housing)

- Overdraft: Yes

- FSCS protected: Yes

As the UK’s largest mutual, Nationwide Building Society is owned by its members rather than shareholders.

It has climate targets and reports on emissions linked to its lending. However, its acquisition of Virgin Money UK means its overall footprint isn’t fully fossil-free.

Best for: A middle ground between ethics and mainstream banking.

4. Cumberland Building Society

- Monthly fee: £0

- Fossil fuel exposure: None

- Positive impact investment: Limited (local community focus)

- Overdraft: Yes

- FSCS protected: Yes

Cumberland Building Society takes a local-first approach, lending within its communities and avoiding complex global investments.

Best for: Simplicity and local impact.

5. Starling Bank

- Monthly fee: £0

- Fossil fuel exposure: No direct project finance

- Positive impact investment: None

- Overdraft: Yes

- FSCS protected: Yes

Digital bank Starling Bank offers strong app-based banking and avoids direct fossil fuel project finance.

However, it doesn’t actively direct money towards positive impact in the same way as mission-led banks.

Best for: Low-cost digital banking with some ethical considerations.

Read our full review of Starling Bank

Other banks people often ask about

- Monzo – avoids direct fossil fuel lending but doesn’t have a full ethical policy

- Al Rayan Bank – Sharia-compliant, but not necessarily fossil fuel-free

Are ethical current accounts safe?

Yes – most ethical current accounts are protected by the Financial Services Compensation Scheme (FSCS).

This means your money is protected up to £85,000 per person, per bank if the provider fails.

Some app-based providers use safeguarding instead, so it’s always worth checking.

How to avoid greenwashing

If you’re trying to work out whether a bank is truly ethical, look for:

- Clear exclusions (e.g. no fossil fuels)

- Detailed reporting on where money is lent

- Independent certifications (such as B Corp or Good With Money’s Good Egg)

- A long-term track record, not just recent marketing

Red flags include vague language, selective disclosures or small “green” initiatives alongside large-scale fossil fuel financing.

Why switch to an ethical current account

Switching your current account won’t change the world overnight.

But it does change what your money supports.

And in a system where banks still play a major role in funding fossil fuels, that choice carries more weight than it might seem.

Looking for more Good Money choices?

If you want a savings account, insurance policy, investment fund or mortgage from companies that do the right thing, check out our Good Eggs.

These are companies that have passed strict independent criteria to show they make a positive impact – for the planet, society and customers.

The Good Money Test is our editorial checklist for assessing financial providers. Our Good Egg is our formal kitemark.

If you want to have a savings account, insurance policy, investment fund or mortgage from companies that do the right thing, check out our Good Eggs.

These are companies that have passed strict (independent) criteria to prove they make a positive impact – to the planet, society, and you.

Why trust Good With Money?

Good With Money is an independent UK-based platform specialising in ethical and sustainable finance. We review financial products based on environmental and social impact as well as financial value.

Good With Money occasionally uses affiliate links to providers or offers, where relevant. This means that if you open an account or buy a service after following the link, Good With Money is paid a small referral fee. We choose our affiliates carefully and in line with the overall mission of the site.