SpaceX’s record-breaking IPO is turning heads on Wall Street, but Good With Money readers have more to consider than the next move in its share price.

This is a company built on rockets, satellites, military contracts, social media and AI. Its arrival on the stock market could become an early test of how sustainable investors handle the next generation of mega-companies.

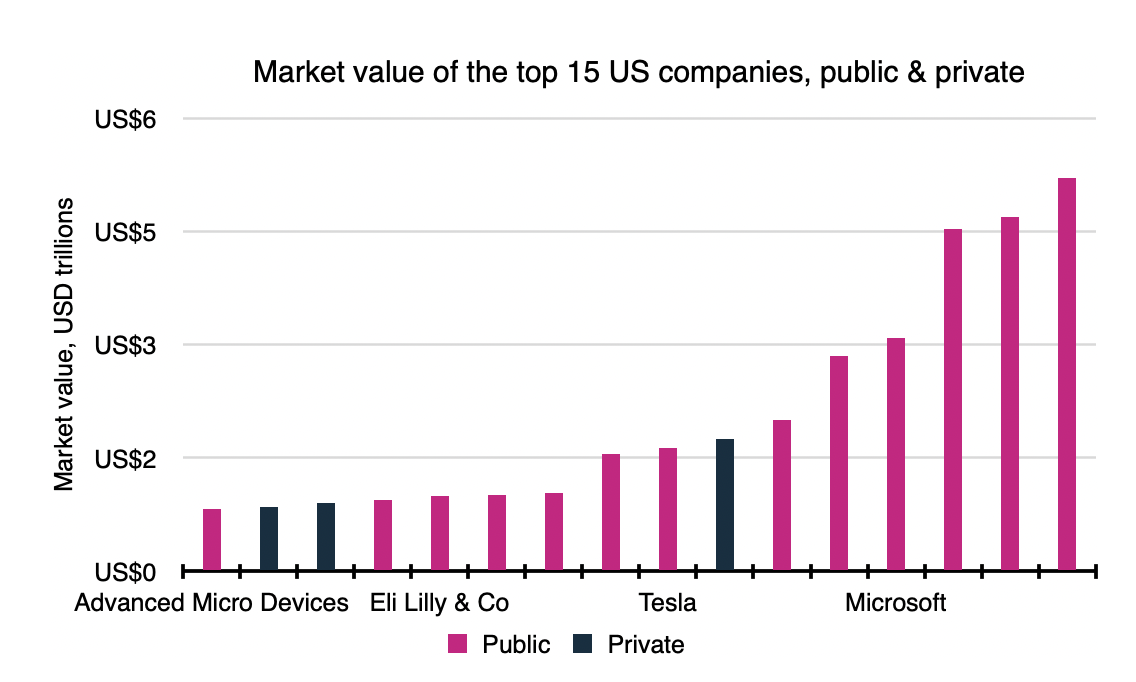

Once huge companies list on the stock market, they can quickly find their way into mainstream funds, pensions and index trackers. In other words, you may end up exposed to them without actively choosing to invest.

SpaceX is not the only one to watch. OpenAI and Anthropic are also preparing for potential stock market listings, bringing artificial intelligence, energy use, governance and social impact firmly into the sustainable investing debate.

Below, Tertius Bonnin, Financial Planner at EQ Investors, looks at what these landmark IPOs could mean, and why the sustainability case is far from straightforward.

Together, their listings could raise more money in 2026 than the US IPO market has ever seen in a single year.

Three of the most talked-about companies in the world are preparing to list on the US stock market. SpaceX, OpenAI and Anthropic – names that you may recognise from rocket launches, ChatGPT, or Claude – have spent years as private businesses funded by venture capital and private equity. Between them, they could raise more money in 2026 than the entire US IPO market has raised in any year on record.

The names behind the numbers

A brief introduction to each may be useful given the private nature of these companies.

OpenAI makes ChatGPT, the chatbot launched in late 2022 that became one of the fastest-adopted consumer products in history. It is on track for around $30 billion (£22.4 billion) in annualised revenue but has told investors it expects to spend roughly $600 billion (£448 billion) before turning a profit at the end of the decade.

Anthropic owns Claude, a rival chatbot that has grown quickly in the corporate market and now generates around $40 billion (£29.8 billion) of annual recurring revenue.

Private valuations are taken from latest publicly disclosed values. Public valuations taken from last market close. Source: Bloomberg, EQ Investors. Data as at 27/05/2026.

A rare window – and why it matters

The scale of these listings is the part worth pausing on.

At the valuations bankers are targeting, SpaceX would come to market at $1.75 trillion (£1.31 trillion) and OpenAI close to $1 trillion (£746 billion), making them larger on day one than any of the famous IPOs that came before.

Visa, Meta, Alibaba and General Motors were the four largest US flotations of the past 30 years. Each raised between $16 billion (£11.9 billion) and $25 billion (£18.7 billion). SpaceX alone is aiming for $75 billion (£56 billion).

Part of what makes this moment unusual is how rare blockbuster IPOs have become. Businesses have stayed private for longer, fewer have come to market, and those already listed have bought back shares or merged with one another. The number of US-listed companies has more than halved since 1995 – a trend that has also been experienced in Europe and the UK.

The result has been a shrinking pool of listed companies. A wave of mega-IPOs reverses that pattern and is likely to result in several new high-profile companies coming to market.

Hype and reality

For most investors, the practical implications are narrower than the headlines suggest.

Those looking to take part in IPOs, particularly those as high profile as these, rarely receive a full allocation at the IPO price. The more important point is how traditional investors’ exposure to themes such as AI or space is set to increase without any deliberate investment decision being made.

Together, SpaceX, OpenAI and Anthropic could well become large constituents of mainstream equity indices like the S&P 500 or the MSCI AC World meaning passive, unscreened investment strategies that replicate index holdings will need to buy meaningful positions.

Much of this will depend on something called the “free float” which measures how much of a company’s equity is considered not tradable. This could either be because it is owned by company insiders (Elon Musk owns around 40 per cent of SpaceX) or because it is held by long-term strategic shareholders.

This can have a material impact on inclusion within indices. SpaceX is coming to market with less than 10 per cent of its equity considered freely floating. This means that despite the eyewatering headline valuation, SpaceX may make up less than 0.20% of indices like the S&P 500 – significantly lower than other public companies with similar headline valuations.

Sustainability considerations

Inclusion of these companies in EQ’s sustainable portfolios will vary and is still being evaluated by all our chosen fund manager partners.

Given their current private ownership, their lower level of transparency in corporate reporting leaves key points of disclosure uncertain. Strong sustainable investment approaches will take decisions on these companies once they have obtained more granular detail on revenue splits, governance models, Environmental, Social and Governance (ESG) targets and strategy plans – all of this will be enabled post IPO.

Nevertheless, at high-level, we see a few key risks and opportunities for the sustainable investor.

SpaceX is the most complex case given its diverse revenue streams. Starlink offers the clearest impact argument, enabling digital connectivity in previously underserved regions, but its military contracts represent a material risk. The social media platform X, the environmental footprint of rocket launches, and the governance of AI engine Grok all carry significant social and environmental concerns. Elon Musk’s governance flag is unlikely to be resolved without a surprising shift at board level.

On ChatGPT and Anthropic: their core revenues, developing AI models, can be classified as a broad enabling technology. This is not inherently impact-aligned in itself; it depends entirely on end-use.

That makes company intent and ESG track-record the key differentiator. Both are currently structured as Public Benefit Companies, but Anthropic leads on AI safety and intentionality, declining military contracts to date being one clear example. Both carry structural challenges, including the high environmental cost of running large models and the risk that their technology is used to enable unsustainable activities.

EQ’s positioning

EQ’s portfolios employ different sustainability approaches and objectives, which may result in different holding decisions across these companies post-IPO. As a result, it is difficult to predict at this stage how each will be positioned.

Our preference is always to maintain the clear dual mandate of our portfolios including both financial and sustainable objectives, while managing the exposure to the long-run opportunity in areas such as responsible artificial intelligence. The themes driving these listings are present in portfolios already, at least in part, just not in concentrated form.