A mortgage is likely to be the biggest financial commitment you ever make, so finding an affordable and suitable deal must come first. But when several lenders offer similar rates and terms, it’s worth looking beyond the headline price at the company behind the mortgage.

Many mainstream banks continue to finance sectors linked to fossil fuels, deforestation and weapons. By choosing carefully, you may be able to find a competitive mortgage while supporting a provider with clearer ethical policies, a mutual ownership model, credible environmental commitments or a fairer approach to customers.

Building societies feature strongly in this list because they are owned by their members rather than external shareholders. This can allow profits to be reinvested in the business or used to benefit customers. Mutual status alone does not make a lender responsible, however, so we have looked at each provider’s policies, transparency, environmental and social impact, and treatment of customers.

Our six picks include five mortgage lenders and one whole-of-market broker. Between them, they cover mainstream borrowing, eco homes, self-build projects, first-time buyers and people who want help comparing lenders on both price and ethics.

Rates and products were checked on 13 July 2026. Mortgage deals can change frequently, and the rate available to you will depend on your deposit, circumstances and property.

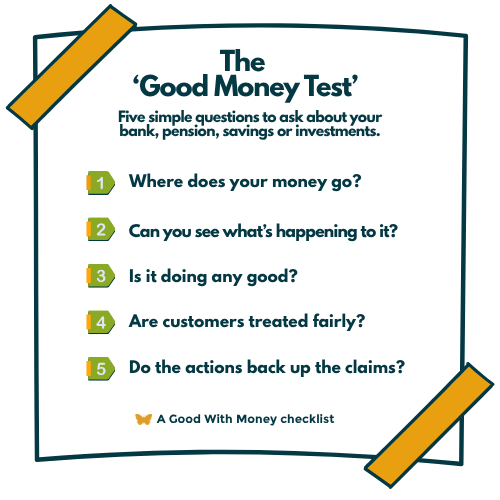

How we use the Good Money Test

We put each provider through the Good Money Test, Good With Money’s framework for assessing whether financial firms live up to their claims.

We ask:

- Where does the money go, and does the provider have clear policies governing its lending and wider business?

- Is it transparent about its rates, fees, ownership and environmental or social impact?

- Does it make a measurable positive contribution to people or the planet?

- Does it treat its customers fairly and offer suitable, accessible products?

- Do its actions and results support the claims made in its marketing?

Mutual ownership, green mortgage products and accreditations such as B Corp status are all positive evidence. None provides an automatic pass. We have also considered current controversies, limitations and gaps in disclosure.

Responsible mortgage providers at a glance:

| Provider | Type | Best for | Good Money Test |

|---|---|---|---|

| Ecology Building Society | Specialist lender | Eco homes and self-builds | Strong pass |

| Coventry Building Society | Mainstream mutual | First-time buyers and remortgagers | Pass |

| Suffolk Building Society | Smaller mutual | Unusual circumstances and individual underwriting | Pass, with reservations |

| Nationwide Building Society | Large mutual | Mainstream borrowing and green improvements | Qualified pass |

| The Co-operative Bank | Ethical bank | Borrowers prioritising lending exclusions | Strong pass |

| WR Ethical | Mortgage broker | Comparing lenders on price and ethics | Strong pass |

Ecology Building Society

Good Money Test verdict: Strong pass

Ecology Building Society remains the top choice for borrowers whose property itself has a strong environmental or social purpose.

It specialises in mortgages for energy-efficient homes, self-builds, modular construction, major renovations, conversions, shared ownership, affordable local homes and community-led housing. It also considers non-standard building methods that many conventional lenders will not accept.

Its current product range includes:

- Eco Home variable rate of 4.69 per cent at up to 80 per cent loan-to-value (LTV)

- Renovation variable rate of 5.19 per cent at up to 80 per cent LTV

- Self-Build rate of 5.69 per cent at up to 65 per cent LTV

- Community Living variable rate of 5.34 per cent at up to 90 per cent LTV

- Shared Ownership variable rate of 4.69 per cent at up to 95 per cent LTV

Some products also include up to £1,000 cashback towards installing a heat pump. Fees, early repayment charges and eligibility vary between products.

Ecology rewards properties that achieve higher energy standards through its C-Change discounts. Its mortgages are funded by members’ savings, giving customers a relatively clear view of how money moves through the society.

It’s a Good With Money Good Egg and Fair Tax accredited.

The limitation is availability. Ecology is unlikely to be the right lender for an ordinary home with no significant environmental features or improvement plans. Its specialist, manually assessed mortgages may also cost more than leading mainstream deals.

Good for: Eco homes, self-builders, major energy-efficient renovations, co-housing and unusual sustainable properties.

Coventry Building Society

Good Money Test verdict: Pass

Coventry Building Society combines the mutual model with stronger-than-average evidence on environmental performance, community investment and customer experience.

The society is a certified B Corp. Its wider group reported a 62 per cent reduction in Scope 1 and 2 emissions compared with 2021, carbon-neutral operations and more than £6 million invested in communities during 2025. Its sustainability strategy covers ethical lending, access to green finance, financial inclusion, vulnerable customers and access to housing.

Existing mortgage customers can access a lower rate when borrowing more for eligible energy-efficiency improvements. Coventry also received a Fairer Finance gold ribbon for mortgage customer experience in spring 2026.

Coventry completed its purchase of The Co-operative Bank in 2025. They remain separate mortgage propositions with different histories and policies, but readers should be aware that two entries in this list now sit within the same group. Coventry’s B Corp certification applies to the building society itself and should not automatically be read across to every part of the enlarged group.

Coventry does not have Ecology’s tightly defined environmental lending purpose or The Co-operative Bank’s long-standing exclusion policy. It earns its place through the combination of mutual ownership, measurable group-level progress, green borrowing and competitive mainstream availability.

Good for: First-time buyers, home movers and remortgagers looking for a mainstream mutual with credible sustainability commitments.

Suffolk Building Society

Good Money Test verdict: Pass, with reservations

Suffolk Building Society is a smaller mutual with a flexible approach to borrowers who may not fit the standard high-street mould. Its range includes mortgages for first-time buyers, self-employed people, later-life borrowers, self-builders, expats and holiday-let owners.

Current residential products include a two-year fixed rate of 5.75 per cent and a five-year fixed rate of 5.69 per cent at up to 80 per cent LTV. At 90 per cent LTV, its current fixed rates are 5.99 per cent for two years and 5.89 per cent for five years. Its Eco Self Build and Renovation mortgage has an initial discounted rate of 5.59 per cent at up to 80 per cent LTV.

Its strongest Good Money Test performance is in community impact. The Safe Homes for Suffolk campaign supports organisations addressing homelessness, social isolation and domestic abuse. Staff receive four paid volunteering hours each month.

The society has installed solar panels and energy-efficient lighting, purchases renewable electricity for its sites and is working towards carbon neutrality in its own operations.

However, we couldn’t find a detailed public policy setting out broad environmental or ethical exclusions across its mortgage lending and financial activities. This makes Suffolk a responsible community mutual rather than a deeply screened ethical lender.

Good for: Borrowers who value individual underwriting, particularly self-builders, first-time buyers, self-employed applicants and people with less conventional circumstances.

Nationwide Building Society

Good Money Test verdict: Qualified pass

Nationwide offers the reach and product choice of a major mainstream lender while retaining mutual ownership.

Its standout environmental product is Green Additional Borrowing for existing mortgage customers. Borrowers can access between £5,000 and £20,000 at zero per cent interest for the first two or five years, provided all the money is spent on eligible energy-efficiency improvements. It’s available at up to 90 per cent LTV and has no product fee. Any balance left after the fixed period moves to Nationwide’s standard mortgage rate unless the borrower switches to another available deal.

Eligible measures include insulation, solar panels, heat pumps, replacement windows, electric vehicle charging points and some water-saving improvements.

Nationwide narrowly missed receiving an eco-bank endorsement in a 2025 Which? assessment. The research found that Virgin Money, which Nationwide acquired in 2024, had limited exposure to companies providing services to the oil and gas industry, representing around one per cent of its business lending.

There are also governance and customer-treatment concerns. Nationwide was fined £44 million by the Financial Conduct Authority in December 2025 for historic weaknesses in its financial crime controls. It has also faced criticism over executive pay and the limited member say on its acquisition of Virgin Money and remuneration decisions.

These issues prevent an unqualified ethical endorsement. Nationwide remains on the list because its mutual structure, wide accessibility and unusually generous green additional borrowing product give it a practical role for borrowers who would otherwise choose a large commercial bank.

Good for: Mainstream borrowers who want a mutual lender, particularly existing customers planning substantial energy-efficiency improvements.

The Co-operative Bank

Good Money Test verdict: Strong pass

The Co-operative Bank has had a customer-led Ethical Policy since 1992. It covers its approach to people, communities and the planet, including restrictions on the businesses and activities it will finance.

A 2025 Which? assessment named it as one of only two banks to earn an environmental endorsement. The research found no exposure to fossil fuels in its banking activities and praised the strength of its ethical standards and emissions reporting.

The bank also gives £5 to youth homelessness charity Centrepoint for every eligible mortgage. Existing mortgage customers can use an Energy Saving Trust tool to create a home improvement plan and may be able to borrow more through its Green Loan for energy-saving work.

The main drawback is access. The Co-operative Bank does not currently offer mortgages to new customers directly. New borrowers must apply through a mortgage broker, while existing mortgage customers can switch deals or explore other options through the bank.

The bank is now owned by Coventry Building Society. Its Ethical Policy remains a distinct reason for inclusion, but the two providers should no longer be viewed as entirely separate corporate groups.

Good for: Borrowers who place particular weight on ethical lending exclusions and are willing to apply through a broker.

WR Ethical

Good Money Test verdict: Strong pass

WR Ethical is a mortgage broker rather than a lender. It earns a place because it helps customers compare lenders’ ethics alongside rates, fees and suitability.

Founded in 2020, the firm offers whole-of-market mortgage advice and says it will tell customers when a cheaper comparable deal is available directly from a lender, even when WR Ethical cannot arrange it itself. It uses research from Ethical Consumer to explain lenders’ environmental and ethical records, while leaving the final decision with the customer.

Its charges are published clearly online. Standard mortgage applications currently cost £295 for new customers and £245 for existing customers. Specialist applications cost £495 and £445 respectively. Like-for-like remortgages, product switches and insurance advice are fee-free.

WR Ethical gives to charity from every application fee and says it aims to donate five per cent of turnover and 20 per cent of profit to charitable causes.

Its latest published impact report, covering 2024/25, said that 57 per cent of its lender business went to Ethical Consumer Best Buys, compared with a national industry estimate of 29 per cent. Thirteen per cent went to lenders it classified as providers to avoid, compared with 34 per cent nationally.

Its statutory accounts for the year ending 31 March 2026 show charitable donations of £15,406 against turnover of £308,126, meaning it met its commitment to donate five per cent of turnover during the year. The accounts are unaudited, as permitted for a business of its size.

WR Ethical became a certified B Corp in March 2026, achieving an overall B Impact score of 94.7, above the 80-point certification threshold. It’s also Fair Tax accredited.

No broker can guarantee that the cheapest suitable lender will also have the strongest ethical record. WR Ethical’s value lies in making that trade-off visible, rather than assuming price is the only factor.

Good for: Borrowers who want personal mortgage advice, transparent fees and help comparing the environmental and ethical records of different lenders.

Should you pay more for a responsible mortgage?

An ethical label should never persuade you to take a mortgage that is unsuitable or unaffordable. Even a small difference in interest rate can add up over a long mortgage term.

Compare the total cost over the initial deal period, including the interest rate, product fee, valuation costs, incentives and any broker charge. You should also consider the lender’s affordability criteria, early repayment charges and likely service.

Where costs are reasonably close, ownership, ethical policies, customer treatment and support for greener homes can provide a useful way to choose between providers.

A mortgage broker can help you compare the full cost and assess which lenders are likely to accept your circumstances. Ask whether the broker searches the whole market, how it is paid and whether it will tell you about direct-only deals.

If you want to have a savings account, insurance policy, investment fund or mortgage from companies that do the right thing, check out our Good Eggs.

These are companies that have passed strict (independent) criteria to prove they make a positive impact – to the planet, society, and you.

Frequently asked questions about responsible mortgages

What is a responsible mortgage provider?

A responsible mortgage provider considers its wider impact on customers, communities and the environment, rather than focusing solely on profit.

This might mean having clear ethical lending policies, supporting greener homes, treating vulnerable customers fairly, investing in local communities or operating as a member-owned mutual. No single label guarantees that a provider is responsible, which is why we assess its ownership, policies, transparency and actions through the Good Money Test.

Are building societies more ethical than banks?

Building societies are owned by their members rather than external shareholders. This means profits can be reinvested in the business or used to benefit members instead of being paid to investors.

That structure is a positive starting point, but it does not automatically make every building society ethical. The strength of its environmental policies, customer treatment, community activity and transparency still matters.

Do responsible mortgages have higher interest rates?

Not necessarily. Mainstream mutuals such as Coventry, Nationwide and Suffolk may offer rates that compete with those available from commercial banks.

Specialist mortgages for eco homes, self-builds or unusual properties can be more expensive because they require individual underwriting and may carry additional risks. Compare the total cost of the mortgage, including fees, incentives and early repayment charges, rather than looking only at the headline rate.

What is a green mortgage?

A green mortgage rewards borrowers for buying an energy-efficient home or making improvements that reduce its energy use.

Benefits can include a discounted mortgage rate, cashback or cheaper additional borrowing. Eligibility may depend on the property’s Energy Performance Certificate rating or on the borrower spending the money on approved measures such as insulation, solar panels or heat pumps.

How can I check whether a mortgage lender is ethical?

Look beyond environmental slogans and check whether the lender publishes clear information about its ownership, lending policies, emissions, community investment and customer treatment.

Independent accreditations and assessments can provide useful supporting evidence, but they should not be viewed as guarantees. Good With Money uses the Good Money Test to examine where money goes, transparency, positive impact, fair treatment and whether a provider’s actions support its claims.

Is WR Ethical a mortgage lender?

No. WR Ethical is a whole-of-market mortgage broker.

It searches for suitable mortgages and helps customers compare lenders’ ethical and environmental records alongside rates, costs and eligibility. The mortgage itself will be provided by the lender ultimately selected by the borrower.